Scope & method. I’m basing this breakdown entirely on materials I captured directly: front-end code bundles, on-page text, and Network/XHR logs. I’m not leaning on outside marketing blurbs or hearsay. Instead, I’ll walk you through Orbion using its own words and behavior—UI states, API calls, and just as importantly, what’s missing (wallet-connect, signature prompts, on-chain transactions, DEX integrations). The aim is straightforward evidence and clear reasoning—no hype, no dramatics.

What Orbion Says It Is

Orbion (domain name: orbion.vip) presents itself as an “Advanced DEX Sniping Bot” for the Solana ecosystem. Across the interface copy and feature panels, the product introduces a familiar story:

Automated trading via a “bot” you can create and manage inside a web dashboard with tabs like Create Bot and My Bots.

A Telegram bot is positioned as an auxiliary control/notification surface.

A simple amount input (peso-denominated) and a “Wallet Balance” readout exist right on the page, implying that once you “fund” your account, the bot will operate on your behalf.

If you stop here, Orbion looks like a slick, consumer-friendly gateway to “hands-free” Solana trading.

What a Real Solana Sniping/Trading Bot Must Do (Baseline)

Before we audit Orbion, here’s the minimum a genuine Solana-native trading/sniping tool must demonstrate:

Web3 Wallet Connection. A Connect Wallet flow (Phantom, Solflare, Backpack, Slope/Sollet, etc.). In code, you’ll typically see window.solana and wallet-adapter patterns.

On-Chain Transaction Prompts. On every buy/sell/snipe, your wallet opens a signature request that includes instructions and fees (lamports). In code, look for primitives like sendTransaction, TransactionInstruction, or VersionedTransaction.

Publicly Verifiable Transactions. After signing, the product shows a transaction signature (hash) so you can click through to Solscan or Solana Explorer.

Program/DEX Interactions. Trades on Solana route through protocols like Jupiter (aggregator), Raydium, Orca, Serum. Real bots leave a paper trail of program IDs and DEX activity.

Token Accounts & Balances (ATA). When you acquire a token, your wallet’s associated token account reflects the new balance; the UI should be a mirror of wallet reality, not a separate ledger.

Keep those five pillars in mind. They’re the difference between blockchain trading and a website that simulates balances.

Forensic Product Audit

Wallet Connection: Absent

There is no “Connect Wallet” button and no adapter UX (Phantom/Solflare/Backpack).

At the code level, there are no references to the Solana wallet surface (window.solana) or wallet/tx primitives (sendTransaction, TransactionInstruction, VersionedTransaction).

You log in and fund an internal account; the page shows “Wallet Balance: ₱0.00” by default—this is an in-platform ledger, not your Solana wallet.

Why this matters: Without wallet connect, the app cannot request signatures or touch your on-chain assets. Whatever “trading” it claims to do, it is not being done by you, under your custody, on your wallet.

On-Chain Prompts & Explorer Proof: Absent

The UI provides an amount input (with a minimum like “min ₱100”) and a “Create Trading Bot” button that can be disabled purely based on your numeric input.

There is no wallet pop-up for signing a transaction, no instruction preview, no fee breakdown—nothing you’d see on any real Solana interaction.

There are no transaction hashes or explorer links surfaced to the user after any action.

Why this matters: Without a signature request and a public tx hash, there is no on-chain audit trail. The app can claim “trades,” but users have no verifiable record.

Program/DEX Activity: Absent

A product calling itself a DEX sniping bot should reveal protocol touchpoints: Jupiter routes, Raydium/Orca/Serum program IDs, pool addresses, or at minimum DEX brand mentions in the UI or code.

The materials you provided do not contain such markers. There’s no sign of aggregator routing, liquidity pool discovery, or program instruction assembly.

Why this matters: Without DEX interactions, sniping is a branding claim, not a function.

Where the Money Actually Flows: Centralized Server APIs

All monetary operations—deposit, withdraw, wallet, dashboard, transactions, investment, subscription, referral commissions—are implemented as HTTP calls to /api/... endpoints. Representative examples include:

Why this matters: This is custodial and off-chain. You are crediting a balance on a database, not moving funds on Solana. The operator controls the ledger and can mint or revoke balances at will.

Deposits: Off-Chain, With Screenshot “Proof”

The deposit flow is telling:

The front-end features a code path that captures a screenshot of your payment proof (e.g., via a toDataURL("image/jpeg", 0.8) pattern) and uploads it to the server through an endpoint such as:

POST /api/deposit-request

Payment settings parse raw addresses (e.g., TRC20:..., Solana:...) to display send-to instructions, consistent with manual transfers, not wallet-connected on-chain flows.

There are no regulated fiat gateways (e.g., Stripe/PayPal), and more importantly, no on-chain tx hash is used as “proof.” The “proof” is literally an image.

Why this matters: In Web3, your signature + the resulting hash is the proof. Screenshots are not proof; they’re support attachments in centralized systems. A genuine Solana app would never ask you to upload a payment receipt image to get credited.

UI Shell Behavior: The “Bot” as a Container

The Create Bot card is a marketing shell with a disabled button until a minimum amount is entered.

The “My Bots” area is a tabpanel container that toggles visibility and shows placeholders such as “Loading your bots…” and “Active Bots (…)” only after the server returns data.

There is no on-chain session state—no positions, no signed instructions, no live route/price/AMM logs—just UI states bound to server responses.

Why this matters: The “bot” is a page section that reflects database state, not a live, on-chain trading process.

Earnings Model

Fixed Daily ROI in the Interface

The interface explicitly promotes fixed daily returns (e.g., “Fixed daily returns on your investment,” “Daily Profit” displayed as 2% in the captured DOM). Elsewhere in the UI text, you’ll find lines like “Up to 2%/3% daily profit potential.”

Why this matters:Fixed daily ROI does not exist in real, market-risk trading. Markets are variable. Any “bot” promising fixed daily yields is not describing normal trading—this is the hallmark of a HYIP (high-yield investment program) structure.

Referral Earnings: “Earn 1% Daily From Referrals”

The interface promotes a 1% daily referral commission and exposes a dedicated API to fetch referral commissions:

GET /api/referrals/commissions

Why this matters: A daily, percent-based referral payout tied to “investment balances” is a strong indicator of a pyramid/Ponzi dynamic, especially in the absence of real on-chain PnL to fund it. Legit affiliate programs pay from real product/service revenue or fees, not from new deposits.

Transparency & Branding

Author metadata and presentation are generic. There are no linked audits, no protocol IDs, no public code, and no demonstration of on-chain trades.

The base page even includes a development-preview banner script from a well-known cloud IDE—its message, in plain language, says this is a temporary development preview“not for public use.”

Why this matters: Money-handling software should not present itself to the public on a dev-preview rail. For a tool that expects deposits, this is a red flag about release maturity and operational discipline.

Consistency Check: Claims vs. Behavior

Let’s compare Orbion’s claims with its observable behavior:

Claim

What You Should See in a Real Solana App

What Orbion’s Materials Show

“DEX sniping bot (Solana)”

Wallet connect; tx signatures; explorer hashes; DEX program IDs

No wallet connect; no signatures; no hashes; no DEX calls

“Automated bot”

Live positions, program interactions, AMM routes

UI shell + server-fetched lists; no on-chain evidence

“Profit sharing / copy trading”

Profit share on actual PnL from your wallet/account

A platform “wallet” (database balance), not on-chain

“Deposit”

Wallet signature or regulated fiat gateway

Manual send + screenshot upload to be credited

The discrepancy is not subtle. The entire money model is centralized and API-driven, while the entire Web3 layer (connect, sign, verify) is missing.

Security & Custody Implications

Custody Risk. Funds reside in a platform-controlled wallet (a database number) until the operator chooses to honor a withdrawal API call. You do not hold the keys; you do not sign transfers.

No On-Chain Rights. Because there are no signatures, you have no transaction-level rights. If balances are modified or withdrawals stall, there is no explorer trail to support your claim.

Manual Proof Flow. The deposit “proof” is a screenshot posted to an API endpoint. This invites disputes and arbitrary crediting logic—again, a custodial pattern where the operator is the judge.

Release Discipline. A dev-preview banner embedded in the main page indicates that the build pipeline is not production-grade.

What This Really Is

Taking all of the above together:

The “DEX sniping bot for Solana” branding is not supported by a wallet connect, on-chain signatures, explorer hashes, or DEX/program interactions.

The UI is a front-end shell: amount input, disabled button logic, a “My Bots” container that shows placeholder text and fills from server data.

The funds model is custodial, with a database “wallet”, API-driven deposit/withdraw, and a screenshot-based deposit proof mechanism.

The earnings model revolves around fixed daily returns and daily referral payouts—classic HYIP composition.

The operational posture (development preview script on the main page) does not align with a product that should be handling public deposits.

Classification: This fits a centralized HYIP/Ponzi-style investment scheme with a sniping/trading bot veneer. It is not a Solana-native trading/sniping product. It operates off-chain, under operator custody, and simulates yield via server-side balances and referral overlays.

How to Self-Verify in Minutes (Optional, For Readers)

If you’re technically inclined, you can replicate the core findings without any special tools:

Open the site and look for a “Connect Wallet” button (Phantom/Solflare/etc.). You won’t find one.

Click any action that claims to trade/snipe/buy/sell. Your wallet should ask for a signature. It won’t.

Open DevTools → Network, perform a “deposit,” and note the requests. You’ll see /api/wallet/deposit and a /api/deposit-request upload with an image/screenshot.

Ask for a tx hash. There isn’t one presented—because no transaction was signed.

Look for DEX routes. You won’t find Jupiter/Raydium/Orca/Serum program traces.

Try withdrawing. It’s an API request, not a signed transaction from your wallet.

Final Analysis & Recommendation

My analysis, constrained to the artifacts you provided, is unequivocal:

Orbion is not a Solana DEX sniping bot in any meaningful, on-chain sense.

Its core mechanics—funding, “profit,” referral payouts—are off-chain, driven by a centralized database via HTTP APIs.

The product’s promises (fixed daily ROI, 1% daily referral) and deposit proof flow (screenshot upload) are canonical HYIP signals.

The absence of wallet connect, signature prompts, transaction hashes, and DEX interaction removes any remaining doubt.

Classification:High-risk HYIP / Ponzi-style scheme masked as a “Solana trading/sniping bot.”

Recommendation: Do not treat this as a Web3 product; do not deposit funds you cannot afford to lose; do not promote it as an on-chain trading tool.

If you are assessing platforms in this space, use the five-pillar baseline (wallet connect, signatures, hashes, DEX interactions, wallet balances) to screen for authenticity.

Closing Thought

Healthy skepticism isn’t cynicism—it’s due diligence. If a “bot” can’t connect to your wallet, can’t ask for a signature, can’t show a tx hash, and can’t name the DEX routes it uses, it’s not a blockchain trading tool. It’s a website that moves numbers in a database.

Table of Contents

Surveyon is one of the more well-known online survey platforms available in Asia, including the Philippines.

Many people are curious if it’s really worth the time, whether the surveys pay fairly, and most importantly—if it’s actually legit or just another scam.

In this blog, I will give you a complete and detailed review of Surveyon based not only on my own script and experience but also with additional research and analysis.

You’ll learn what Surveyon is, how to earn points, what the features are, the pros and cons, potential red flags, and my final verdict on whether it’s truly legit.

What is Surveyon?

Surveyon is a legit online survey panel and mobile application operated by dataSpring, Inc., a global market research company under the INTAGE Group.

The app allows users to answer market research surveys and earn points that can later be redeemed via PayPal or gift vouchers.

Unlike shady apps that make unrealistic promises, Surveyon has been operating for years across Asia, with offices in Tokyo, Seoul, Shanghai, Singapore, Los Angeles, London, and Manila, Philippines.

The company behind it is established in the research industry, which is a positive sign.

How Can You Earn Points?

Surveyon offers several ways to collect points:

Events – Special campaigns that give extra points when you participate.

Surveys – The main way to earn. You get invited to answer market research surveys, and in some cases, you earn small points even if you get screened out.

Quickpoll – Daily micro-polls where you can quickly answer a single question and earn points.

Daily Check-In – Simply logging in gives you points.

Referral Program – Invite friends using your code and earn bonus points.

Minimum Withdrawal and Payout

Points Conversion: 10,000 points = around US$1.

Minimum Cashout: Depending on your region, the minimum redemption is 10,000–20,000 points (US$1–US$2). For PayPal, many users report 20,000 points as the actual threshold.

Processing Time: The app claims withdrawals are processed within 3 days, but in reality, it may take up to 7–10 business days depending on the option and country.

So yes—you can earn money, but the actual value per survey is low. Most surveys give 200–1,000 points, which means you’ll need to complete anywhere from 10 to 50 surveys just to reach $1.

Features

Available on Android, iOS, and browser, making it flexible.

Daily Check-In and Quickpoll for consistent small earnings.

Lucky Draw and seasonal events.

Referral bonus system.

Multiple redemption options (PayPal and vouchers).

Data Safety: Encrypted in transit, with options to request account deletion.

Pros of Surveyon

✅ Legit and safe – Backed by dataSpring, a real research company. ✅ Free to join – No need to pay or invest. ✅ Low threshold – You can cash out from $1–$2. ✅ Fast payouts (sometimes as quick as 3 days). ✅ Daily availability – Check-ins and quickpolls provide steady small points. ✅ Consolation points when screened out of surveys.

Cons of Surveyon

❌ Low earnings – Surveys pay little; you need dozens to reach even $1. ❌ Survey disqualification – If your answers are inconsistent, you may get fewer invites. ❌ Mixed reviews – Google Play rating is 3.9★; Trustpilot shows 2.5★. Some users complain about account suspension or missing rewards. ❌ Country-dependent availability – More surveys in some countries, fewer in others. ❌ Not sustainable as income – This is clearly a micro-earning app, not a job.

Warnings

Account deactivation complaints: Some users claim their accounts were flagged right before withdrawal. While this isn’t widespread, it’s a risk.

Inactivity policy: If you don’t log in for a year, your account may be deactivated.

Referral spam: Avoid random “get rich quick” ads online using Surveyon’s name. The real developer is dataSpring, Inc.

These are not outright scams but things you should watch out for.

Analysis: Is Surveyon Legit or a Scam?

Based on my review and all the information I gathered:

Surveyon is a legit platform. It has a registered company behind it, real app listings on Google Play and App Store, and actual payout proofs from many users.

But earnings are very small. Even if you qualify for many surveys, the average payout is just a few cents per survey. At best, you can make a few dollars per month.

It’s not a scam, but it’s also not a reliable income source. Think of it as a micro-earning side hustle, good if you want to make coffee money or test how survey apps work.

Final Verdict: ✅ Legit and Safe Yes, Surveyon is legit and safe to use. It won’t scam you, and it really pays out, but don’t expect significant money. Use it only for small extra earnings, not as a main source of income.

Surveyon is an honest survey app that really pays, but only at a very low rate. If you want to try it out, you can register for free, use daily check-ins and quickpolls, and redeem via PayPal once you reach the threshold.

But here’s the truth: If you are looking for serious money, this isn’t for you. If you’re happy with small rewards, then Surveyon can be worth your time.

Now I want to ask you: Have you used Surveyon? Did you earn anything from it? Share your experience in the comments—I’d love to know what you think!

Table of Contents

Scope and Evidence Inventory

This analysis is grounded in first-party technical artifacts originating from the platform itself:

Production JavaScript/i18n bundles from the running web app (Vue SPA).

Compiled API wrapper modules visible in the app’s loaded scripts.

Live API responses captured via the browser’s Network panel (e.g., “line configuration” JSON and market-list JSON).

SPA entry references (Vite/ESM).

Trading UI DOM capture (K-line canvases; Limit/Market forms; “Seconds”/binary components).

Earlier contextual notes we discussed (e.g., social/WHOIS chatter) are kept to a minimum; the core of this review is the code and the live network traffic produced by the application itself.

The SPA is built with Vue + component libraries (you’ll see Element/Ant patterns in the DOM), and a canvas-based K-line chart renders OHLC candles and volume.

How the App Chooses Its Backend (“Line Config” + Remote Switching)

On boot, the SPA fetches a remote JSON configuration that declares:

One or more API base URLs (called “lines”),

Log endpoints (for telemetry),

Customer service endpoints,

App download links, etc.

A representative API line returned by this config is:

https://epi.nz558.com

The front end then binds all REST calls under a common prefix:

/forerest

and proceeds to query:

Market data (e.g., POST /forerest/kline/find),

Spot endpoints (/forerest/spots/...),

Seconds endpoints (/forerest/second/...),

Identity/wallet endpoints, and so on.

Why this matters: the app does not directly call Binance/OKX/Coinbase/CoinGecko/Chainlink/Pyth from the browser. It gets all market data and executes all orders via its own API line. This is the foundation of the “closed-loop” conclusion later.

Aliyun OSS Remote JSON (Infra Rotation)

The line JSON is hosted on OSS (Aliyun) and can be swapped at will. That enables the operator to:

Rotate API hosts/domains quickly,

Swap log and customer service lines on the fly,

Continue service even if a particular domain is blocked/taken down.

Operationally, this is a hallmark of systems that want flexible domain usage. On its own, it’s not “proof of wrongdoing,” but in combination with the next sections, it becomes a significant risk indicator.

Market Data: The K-Line Chart Is Fed by the Operator’s Own Endpoint

The SPA includes a K-line helper that posts to /forerest/kline/find:

const BASE = "/forerest";

function getKline(payload) {

return http({

url: `${BASE}/kline/find`,

method: "POST",

data: payload

});

}

Real captured responses for the market list/tickers show payloads like:

Critical implication: whatever prices you see in the chart come from their server. There is no front-end connection to public exchange feeds. If they choose to differ from public marks, the UI will still display their price.

Spot Trading: Entirely In-House (Add/Cancel/List via /forerest/spots/...)

All Spot actions in the UI call in-house endpoints:

const SPOTS = "/forerest/spots";

function addOrderSpots(body) {

return http({ url: `${SPOTS}/order/add`, method: "POST", data: body });

}

function getOrderPage(body) {

return http({ url: `${SPOTS}/order/page`, method: "POST", data: body });

}

function cancelOrder(body) {

return http({ url: `${SPOTS}/order/cancel`, method: "POST", data: body });

}

function getSpotsBalance(params) {

return http({ url: `${SPOTS}/wallet/balance`, method: "GET", params });

}

UI forms (as seen in your DOM capture) implement:

Limit order: editable “Price (USDT)” and “Amount (BTC)” inputs.

Market order: price field disabled with “Market order” placeholder; amount in BTC or USDT depending on side.

What you don’t see: a front-end call sending the order to a public venue. Everything is posted to their/forerest/spots/... endpoints.

“Seconds” (Binary-Style): Also In-House (/forerest/second/...)

The seconds/binary module exposes a complete mini-lifecycle:

const SECONDS = "/forerest/second";

function getCycles() {

return http({ url: `${SECONDS}/cycle/findAll`, method: "GET" });

}

function addSecondsOrder(body) {

return http({ url: `${SECONDS}/order/add`, method: "POST", data: body });

}

function getSecondsOrderPage(body) {

return http({ url: `${SECONDS}/order/findPage`, method: "POST", data: body });

}

Risk characteristics of “Seconds”:

Short cycle (e.g., 30s/60s) UP/DOWN wagers.

One tick determines win/loss.

With a closed price feed, settlement is not validated against a public mark/index.

Historically, this UI pattern is associated with high complaint volumes when payouts hinge on a proprietary last-tick.

Real-Time Layer (Socket.IO): Their Server, Not a Public Market Stream

The SPA initializes Socket.IO against the active host. There is nowss://stream.binance.com/... or similar in the front-end. This means:

Real-time “ticks” and order updates are pushed by their infrastructure.

You cannot assume any alignment to public orderbooks or funding marks.

Assets (Recharge/Withdraw/Transfer): No On-Chain Verifiability Hooks in the UI

The UI language is USDT-heavy, yet the front-end lacks:

Chain selectors (e.g., TRC20 / ERC20 / BEP20),

TXID columns,

“View on Explorer” links (Etherscan/Tronscan/BscScan).

You do see generic phrases like “Third-party Withdraw”, “USD Withdrawal”, “Withdrawal Fee”, “Binding Withdrawal Address.” But the necessary scaffolding a real on-chain flow uses (TXIDs, chain labels, explorer links) is not present in the UI.

Why this matters: even if payouts occur “behind the scenes,” production UIs typically reserve placeholders for TXID/Explorer so that a user can verify a transfer cryptographically. The absence of these hooks strongly suggests a ledger-only model where credits/debits are updated internally without public proofs.

Staking (Current Label) vs. Cloud-Mining (Legacy Module Still Present)

The current interface uses “Staking” wording, but the codebase still contains a Cloud Mining module with endpoints like:

GET /forerest/cloudmining/confInfo

POST /forerest/cloudmining/order/buy

POST /forerest/cloudmining/findPage

POST /forerest/cloudmining/order/findPage

POST /forerest/cloudmining/income/findPage

This is textbook white-label behavior: toggle product names/skins while keeping the same deposit-driven yield scaffolding. Again, there are no on-chain proof hooks on the front-end to validate “earnings.”

Invite / Agent / Team Rebate: Heavily Emphasized

Strings and components indicate:

Invite/commission mechanics (“earn cashback when friends deposit”-style copy),

Agent Center, Agent Bill Settlement,

Daily rebate settlement at 00:00 Beijing time.

In regulated contexts, referral tooling is usually ancillary. Here, the referral/agent layer is central, tied to deposits and “activity” modules (lotteries, bonus events). This aligns with high-risk monetization patterns.

Marketing Claims: “100% Deposit Guarantee” Without Concrete Insurance/Regulator Proof

The production copy includes an explicit “100% deposit guarantee” and “compliant digital asset trading license.”

No insurer name, policy number, coverage limits, exclusions, or regulator portal link is integrated into the UI.

No verifiable document viewer in the app that users can click to confirm coverage.

Bottom line: a high-impact claim with no discoverable evidence in the product is a major red flag.

Mixed Branding Blocks in Production (White-Label/Recycled Copy)

Within the production copy, blocks referencing other exchange brands appear. In a properly maintained and regulated production build, unrelated brand copy should never ship. Mixed branding is one of the clearest fingerprints of a recycled/white-label codebase deployed under different skins.

Anti-Inspection UX and Dev Leftovers

Multiple event handlers block right-click and selection/inspect (e.g., addEventListener("contextmenu", ...) with preventDefault() calls).

Development leftovers (e.g., localhost, generic BaseURL placeholders) appear in a production build.

Component class names like BetButton show through in trading buttons.

None of these alone proves fraud; together with the closed data/exec pipeline and the product mix, they depict a stack that does not prioritize transparency.

The DOM You Pasted: What It Confirms

Your DOM snippet shows:

A K-line container (id="k-line-chart") with layered <canvas> elements,

Timeframe toggles (1m, 15m, 30m, 1h, 4h),

Two forms (Limit/Market) with USDT as the pricing unit and BTC as the asset unit,

Quick percentage buttons (1% / 25% / 50% / 100%),

Action buttons styled with classes like BetButton.

This proves that the UI indeed renders a familiar exchange-like surface. Paired with the code and network behavior above, we can say with confidence: the surface is exchange-like, but the data and orders are closed-loop.

“Live Trading” vs. “In-House Simulation”

All browser-side evidence points to “in-house”:

The front end posts to /forerest/kline/find (their server) for chart data.

The spot/seconds orders post to /forerest/spots/... and /forerest/second/... (their server) for placement, listing, and cancellation.

The WebSocket/Socket.IO stream is theirs, not a public market stream.

There are no front-end calls to Binance, OKX, Coinbase, CoinGecko, Chainlink, Pyth, or similar public data/index providers.

There are no index/mark/funding disclosure pages typical of regulated derivatives.

Translation: prices and settlements are whatever their backend says. You cannot independently verify a trade/fill/settlement against a public orderbook or a published mark index, especially critical for “Seconds” where a single tick flips the outcome.

Self-Checks You Can Perform (No Deposit Required)

DevTools → Network while viewing the chart. You will see POST /forerest/kline/find to the active line host (e.g., https://epi...). You will not see public exchange API calls.

One-to-three-minute side-by-side price logging Log last price at Opalp and at a major exchange. If you observe persistent drift/lag beyond normal spread/latency, you’re watching an internal stream.

Look for “Index/Mark/Funding” pages In transparent derivatives products, these are always documented. Absence is a strong tell.

Check withdrawal UI for “TXID” / “View on Explorer” placeholders Even accounts with no history will typically show columns reserved for on-chain proofs. If these hooks don’t exist in the UI framework, assume no cryptographic accountability.

Risk Synthesis (Why This Stack Is Dangerous)

Closed-loop data and execution: all price and order flows are inside the operator’s infra.

Binary “Seconds” + deposit-tied rebates: a classic pattern of rapid loss and recruit-driven cash flow.

Line switching via remote JSON: enables rapid domain rotation.

No on-chain proofs: a USDT-centric UI with zero chain labels/TXIDs in the front end.

Mixed branding: third-party brand blocks in a production build.

Unsupported “100% deposit guarantee”: no insurer, no policy, no regulator link.

Anti-inspection UX + dev leftovers: poor transparency posture.

Each item would be concerning; together they justify a do-not-deposit stance.

Practical Advice If You Already Have Funds There

Attempt the smallest possible withdrawal immediately. Require a TXID and a chain label (TRC20/ ERC20/ BEP20). If they refuse or stall, treat that as critical.

Preserve evidence: screenshots of balances, orders, any chat or email correspondence, and (if you know how) a HAR export of the network panel.

Consider reporting to the proper authorities (e.g., NBI Cybercrime, PNP-ACG, SEC Philippines).

If you funded via card or fiat rails, consult your bank/issuer about a dispute/chargeback.

From a technical and risk-control perspective, this platform does not meet the bar for a legitimate exchange:

The front end never touches public market APIs or indexes; all data and orders are in-house.

The product mix (especially “Seconds”) relies on their last tick, with no independent check.

On-chain verifiability is absent at the UI layer.

Operational patterns (line switching, heavy invite/agent rebates, mixed branding, anti-inspect UX) add to the risk.

The “100% deposit guarantee” claim is unsupported by any verifiable documentation.

Final stance: Treat Opalp.com as high-risk / behave-as-scam. Recommendation:Do not deposit. If already exposed, try a small, immediate withdrawal and insist on TXIDs. Escalate if they cannot or will not provide verifiable on-chain proofs.

Table of Contents

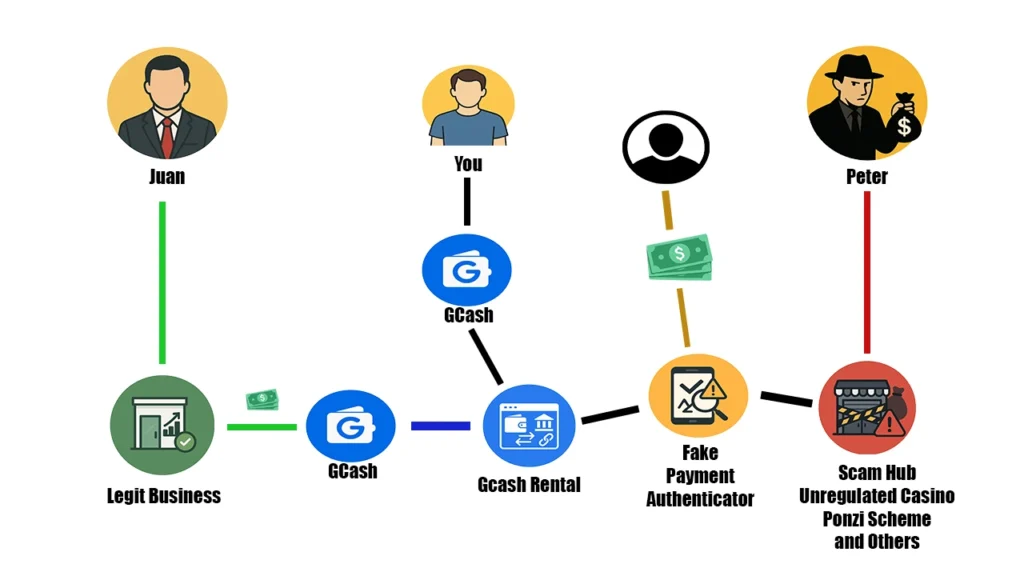

Let’s talk about this new so-called online earning opportunity that has been circulating lately — GCash Rental, sometimes also marketed as Self Rental.

For those who still don’t have any idea what this is, let’s break it down:

What is GCash Rental?

GCash Rental refers to the act of “renting out” or “allowing someone else to use” your GCash account through third-party platforms like HDPay in exchange for daily profits.

The idea is simple:

You deposit money into your GCash account.

You connect your account to their system.

The third-party platform uses your account to move money in and out.

In return, they promise you 1% to 2% daily profit.

At first glance, it looks like passive income: you don’t need to do anything — just put money in your GCash account, connect it to HDPay or similar apps, and wait for your money to “grow.”

How Much Can You Earn?

It depends on the rate set by the platform. Most of these sites advertise 1% to 2% daily return.

If you have ₱10,000 in your GCash, they claim you can earn ₱100–₱200 daily.

In a month, this supposedly adds up to ₱3,000–₱6,000.

If you put ₱100,000, you could “earn” ₱30,000 or more per month.

It sounds attractive, especially to those looking for “easy money.” But before you get tempted, the important question is:

Is this legal?

The Straight Answer: No, It’s Not Legal

The income you see from GCash Rental does not come from legitimate sources. It is connected to illegal activities and is part of a Money Laundering Scheme.

How Does GCash Rental Actually Work?

Let’s use an example:

Meet Juan and Peter

Juan has a legitimate business. It’s properly registered, complete with permits from the Mayor’s Office, BIR, SEC, or even PAGCOR. Everything is legal on the surface.

Peter runs illegal operations — scam hubs, unregulated online casinos, shady lending apps, phishing sites, Ponzi schemes, and more.

Peter needs Juan’s help to move money, but here’s the problem: If Juan and Peter transact directly, they will get flagged under AMLA (Anti-Money Laundering Act). It will be traceable, and both could be charged.

So, what do they do? They use a third-party layer — this is where GCash Rental platforms come in.

Where Do You Come In?

You, the ordinary user, get lured in by the promise of 1% to 2% daily passive income.

You provide your GCash account.

You deposit money as a “float” (₱1,000, ₱10,000, etc.).

The rental service connects your account to a Fake Payment Authenticator.

This Fake Payment Authenticator is used by:

Unregulated gambling operators

Scam hubs

Phishing websites

Ponzi and pyramid schemes

Dating scams, text scams, crypto fraud, and other illicit businesses

When people send money to these illegal hubs, the funds are funneled into your GCash account (alongside hundreds of other rented accounts). But the money doesn’t stay with you.

Once it enters, it’s quickly transferred out to other accounts.

The flow creates a chain that eventually reaches Juan’s legal business.

In Juan’s books, it shows up as consultancy fees, e-commerce sales, marketing revenue, coaching, seminars, etc.

By the time it reaches Juan, the money looks clean — even though it came from scams.

This is Classic Money Laundering

The process perfectly fits the Money Laundering Cycle:

Placement – Dirty money enters the financial system via rented GCash accounts.

Layering – It is moved through multiple accounts to obscure its origin.

Integration – It reappears in Juan’s legal business as legitimate income.

You are essentially serving as a money mule — a bridge for illegal money to move.

Why There Is No Such Thing as Legitimate GCash Rental

Some people ask: “Isn’t there at least one GCash Rental platform that’s legal?”

There is no such thing as a legitimate GCash Rental. Every platform offering it is part of an illegal network tied to scams, unregulated gambling, and fraud.

The promise of 1% to 2% daily return is the bait. The reality: you risk losing your money, your account, your reputation, and your freedom.

So ask yourself:

Is it worth earning a few pesos daily while becoming part of a scam that victimizes thousands of Filipinos?

Is it worth risking jail time, frozen accounts, and criminal records?

The wise answer is simple: Stay away. Don’t rent your GCash. Don’t be a money mule.

Do you think it’s worth it just because of the promised returns?

Or do you agree that it’s a trap that should be avoided?

Drop your opinion in the comments — let’s spread awareness so fewer people fall into this scam ecosystem.

Table of Contents

Today, we are going to take a deep dive into a platform that has been making rounds online, especially here in the Philippines. Its name? DUOB TOP.

Here are the domains connected to DUOB TOP:

duob.top – the primary domain promoted as the official site

duobapp1ye.top – a commonly used referral and login domain

duobaa84.top – an alternate domain likely kept as a backup

The big question is: Is DUOB TOP a legitimate and honorable way to earn money online, or is it simply another elaborate scam waiting to collapse?

Let’s answer that question thoroughly, step by step.

What Exactly Is DUOB TOP?

According to its official website and marketing materials, DUOB TOP claims to be an AI-driven GameFi platform.

The central idea they are trying to sell is that their platform’s main “products” are so-called game equipment or game props. They want users to believe that these props are traded as GameFi assets, similar to NFTs, characters, skins, virtual lands, or special items used in various games.

The platform even throws around the names of popular titles such as GTA, Dota 2, World of Warcraft, and Genshin Impact to make their business sound connected to legitimate gaming ecosystems. The claim is that DUOB TOP sources these digital items, trades them internationally, and then distributes profits back to investors.

But the question is: Is any of this actually true?

The Harsh Truth About “Game Props”

The answer, unfortunately, is no.

All of these so-called “game props” that DUOB TOP showcases on its website and in its app are nothing more than a front. They are unrelated to how the platform actually generates money for its members. In fact, they are fake, non-functional items designed solely to give an illusion of legitimacy.

They do not exist in actual games.

They cannot be minted on a blockchain.

They cannot be bought, sold, or transferred like real NFTs.

There are no smart contract addresses, no API integrations, and no transaction history that would prove these items are authentic.

In other words, the game items being displayed are fake digital assets with zero value.

The games themselves—GTA, Dota 2, WoW, Genshin—have no partnerships or integrations with DUOB TOP. The platform merely invokes these names to appear credible.

If the Game Items Are Fake, Where Does the Money Come From?

This is the critical question.

If the so-called “game items” are fake, then where does the profit promised to investors actually come from?

The reality is: All of the profit being distributed in DUOB TOP comes directly from the deposits of new investors.

The platform is not generating income from any real product or service. It is simply moving money around. Early investors get paid with the money from newer investors, while the platform operators and recruiters skim their share off the top.

This structure is the classic definition of a Ponzi scheme.

Red Flags Everywhere

Over the course of my investigation, I found several red flags that reinforce the conclusion that DUOB TOP is a scam. Let’s go through them one by one.

🚩 Red Flag #1: Unrealistic Returns

DUOB TOP claims you can earn up to 135% profit in just 30 days.

They advertise multiple “investment products.”

For example: their AI Robot plans promise daily profits of 1.8%, 3.5%, and even 5% per day.

They also hold flash sales where you can supposedly lock in even higher daily returns.

If you do the math, these figures are astronomical and completely unrealistic in any legitimate financial market.

No real business, no stock market, no crypto trading bot, and no GameFi project can guarantee such daily profits consistently. These are classic Ponzi promises designed to lure in greed-driven investors.

🚩 Red Flag #2: “No Risk, 100% Security” Claims

Another immediate warning sign is their marketing language.

They boldly declare that DUOB TOP investments are “No Risk” and provide “100% fund security.”

This alone is a dead giveaway of a scam.

Why? Because no legitimate financial or investment platform in the world can guarantee zero risk. The moment you see a company promising no risk and guaranteed profits, you should automatically assume it’s fraudulent.

🚩 Red Flag #3: Pyramid Referral Structure

DUOB TOP heavily emphasizes recruitment. Their compensation plan rewards you with:

8% commission from direct recruits (Level 1)

4% from recruits of your recruits (Level 2)

2% from Level 3 recruits

This is not a standard affiliate marketing model. In legitimate affiliate programs, commissions are tied to the sale of actual products or services.

In DUOB TOP, commissions are tied only to deposits made by new members.

That makes it a pyramid scheme, which is inherently unsustainable. The system only works as long as there are endless new recruits continuously putting in money. Once recruitment slows down, the entire scheme collapses.

🚩 Red Flag #4: Fake Features – Contests, Game Props, and Trading

Inside the platform’s app, you will see flashy tabs labeled “Contest,” “Game Props,” and “Trade.”

The Contest tab lists esports matches with famous teams like G2 Esports and Edward Gaming. But these are fake displays. There are no live odds, no integration with esports APIs, and no betting engine behind the scenes. It’s just a UI façade.

The Game Props tab shows supposed NFT-like items but, as explained earlier, they are non-existent.

The Trade tab is also just a front—visual elements with no actual trading functionality.

All of these are decorations to make the app look sophisticated, when in reality they have nothing to do with how money is moving inside the system.

🚩 Red Flag #5: Fake Licenses

DUOB TOP proudly showcases certificates such as a Colorado business registration and an MSB printout from the U.S. Treasury’s FinCEN website.

Here’s the truth:

A Colorado Secretary of State filing is simply a business registration. Anyone can file one online—it does not authorize investment activity.

An MSB listing is not a license, and FinCEN explicitly warns that scammers misuse these registrations to make it seem like they are regulated.

Therefore, their displayed licenses are misleading props—not proof of legitimacy.

🚩 Red Flag #6: White-Label Code and Template Design

Upon analyzing DUOB TOP’s code, it became clear that the platform is built on a white-label template.

The code contains leftover betting and gambling terms such as bet, odds, matches, and live detail.

The app is connected to unrelated APIs (uunn.org), revealing that it was not built uniquely for DUOB.

The modules are generic—investment, wallet, recharge, withdraw, rebate center—exactly what you find in hundreds of scam templates circulating online.

This contradicts their marketing story of having a sophisticated proprietary AI trading system.

How Recruiters Make Money

To push the scheme, DUOB TOP incentivizes recruiters:

Recruit one person who deposits ₱2,000 → you earn ₱180.

Recruit three → ₱550.

Recruit five → ₱900.

On top of these small recruitment bonuses, DUOB TOP also promotes what they call a “Team Development Monthly Salary.”

At first glance, it looks like a structured job compensation plan with salary levels, but in reality, it is simply another way to push members into nonstop recruiting.

The so-called salary is based entirely on the size of your team and the deposits made by those recruits:

V1 – 5 direct members → ₱2,000

V2 – 13 direct members → ₱9,000

V3 – 28 direct members → ₱17,000

V4 – 150 team members → ₱36,000

V5 – 250 team members → ₱53,000

V6 – 500 team members → ₱117,000

V7 – 1,800 team members → ₱310,000

V8 – 5,000 team members → ₱610,000

While these numbers may look attractive, the “salary” is not backed by any real product or legitimate service.

It is completely dependent on constantly recruiting new members and ensuring they deposit money into the platform.

In short, it’s a fake job structure—a pyramid scheme disguised as a career path, designed to keep people chasing bigger teams instead of recognizing that the entire system has no genuine source of income.

But again, all of this income is funded only by new deposits. There is no real product generating profit.

Why It Will Collapse

DUOB TOP is sustained only as long as new investors keep joining. The moment recruitment slows down, the system will no longer have enough incoming funds to pay out profits.

When that happens, the operators will simply shut down the website, disappear with the money, and leave thousands of members with heavy losses.

This is the destiny of all Ponzi and pyramid schemes, and DUOB TOP is no different.

It is a Ponzi scheme disguised as a GameFi platform. It offers no real products, no real services, and no genuine connection to the gaming industry. It survives only by recycling new deposits into fake profits.

Sooner or later, this platform will collapse, and investors will lose their money.

My advice: Do not invest. Do not promote it. Do not recruit others into it.

Now It’s Your Turn

What do you think about DUOB TOP?

Do you honestly believe it’s a legitimate way to earn money online?

Have you actually earned from it—and more importantly, were you able to withdraw?

Or do you now see it for what it truly is: a dangerous scam preying on unsuspecting investors?

Leave your thoughts in the comments below. Share your experience so that others can learn from it. By speaking out, you can help prevent more people from falling victim to this Ponzi scheme.

📌 Final Word: Always remember, when a platform promises high returns with no risk, guaranteed profits, and commissions based only on recruitment—it is not an opportunity, it is a trap.

Table of Contents

In the world of online trading, hundreds of platforms promise life-changing profits, smart AI strategies, and “guaranteed returns.” Unfortunately, most of them vanish overnight, leaving investors with nothing but frustration and loss.

Today, let’s talk about one of the most talked-about names circulating in forums and social media recently — Precise Planning. If you take a closer look, you’ll see that this so-called platform isn’t just operating from a single website. Instead, it relies on a network of interconnected domains and servers that make up its entire trading ecosystem.

All of these domains are tightly connected and controlled by the same operators. Instead of drawing data from the real crypto market, every feed and chart inside these sites is hard-coded and manipulated to create the illusion of genuine trading activity.

Many people ask: 👉 Is Precise Planning a legitimate trading platform? 👉 Or is it just another well-designed scam disguised as a trading opportunity?

Let’s break this down step by step and uncover what’s really happening behind the curtain.

What Is Precise Planning?

According to its official marketing website, Precise Planning claims to be a regulated global trading platform that was founded in 2007. At first glance, that statement looks impressive — over a decade in the industry, supposedly regulated, and positioned as an established leader.

But is this true? Does Precise Planning really have that kind of history, infrastructure, and transparency?

Spoiler: The answer is no.

Let’s go deeper and examine the red flags that clearly indicate why Precise Planning is not only fake, but also a Ponzi scheme in disguise.

Why Precise Planning Is a Fake Trading Platform

I personally classify Precise Planning as a fake trading system and a Ponzi-style scam. Here are the critical reasons why:

🚩 Red Flag #1: Synthetic Market Feed and Controlled Data

In real trading platforms like Binance or Bybit, the price feeds, order books, and trade executions are live and transparent. They are directly connected to actual markets. Anyone can verify these feeds through APIs or third-party tools like TradingView, CoinGecko, or CoinMarketCap.

But in Precise Planning, everything is hard-coded. The price charts, candlesticks, trade signals, and “market movement” are all synthetic simulations generated by their own servers.

Here’s how it works:

They use three internal servers to simulate trading:

API server – handles buy/sell requests inside the platform.

WebSocket (WS-URL) – pushes real-time fake updates to users.

Kline Chat server – generates the price chart you see on-screen.

Because everything is server-controlled, they can manipulate data at will:

Delay the price feed.

Adjust candlestick patterns.

Remove volume variables.

Change mark price vs. last price.

For example, the price of BTC/USDT in Binance may be $60,000. Precise Planning could delay the data by 2 minutes, feed you a signal “Buy Now,” and when you look at the delayed chart inside their platform, it aligns perfectly. This makes you believe the strategy works, when in reality it’s all pre-scripted manipulation.

This is the biggest sign of fakery — there is no transparent, verifiable matching engine or live market connection.

🚩 Red Flag #2: Fake AI Trading and Unrealistic Plans

Precise Planning proudly promotes its “AI Smart Trading” and different investment plans. The bigger your deposit, the higher the fixed percentage they promise you — sometimes 30% to 60% returns.

Why is this a problem?

No real AI can guarantee fixed profits. Markets are unpredictable. Even the most advanced AI-powered hedge funds cannot lock in guaranteed daily or monthly returns.

Lock-in periods are a scam tactic. Precise Planning forces you to lock your funds for days, weeks, or months. Legitimate bots and strategies don’t require lock-ins — you can stop them anytime.

Activation fees are nonsense. Real trading platforms like Binance never charge an “activation fee” to start trading with bots or strategies. They earn from trading fees, spreads, or commissions — not upfront fees.

Pre-computed profits in code. Inside Precise Planning’s system, your “AI profit” is already calculated. This proves they’re not executing trades — they’re just displaying numbers.

Bottom line: Their so-called AI is just a smokescreen to justify their Ponzi structure.

🚩 Red Flag #3: No Real Market Execution

Looking deeper into the platform code, there is no genuine market execution happening:

No connection to any real exchange.

No trade history that can be verified.

No order book with live buy/sell activity.

No integration with actual liquidity providers.

What you see on screen are fake trades designed to trick you into believing you’re participating in the market. In reality, your money is just circulating within the platform’s internal system.

🚩 Red Flag #4: Recruitment-Based “Invite Gate”

Legitimate trading platforms allow you to trade immediately after registration and funding your account.

Precise Planning, however, uses an invite-to-trade system:

To unlock trading, you must invite 1–9 new investors.

Invite 10–19 people, and you get 14 days of “trading access.”

Your ability to “trade” is directly tied to recruitment.

This is a classic Ponzi model. Real trading has nothing to do with recruitment. If a so-called platform forces you to recruit to gain access, it’s not trading — it’s multi-level scamming.

🚩 Red Flag #5: Referral Commissions from Deposits

In Binance or any regulated exchange, referral commissions come from trading fees your referrals pay when they make real trades.

But in Precise Planning, commissions are taken from the deposits of new recruits. Worse, they allow commissions to flow up to multiple levels, forming a pyramid scheme.

This proves there’s no real revenue model except new money funding old participants. Once recruitment slows down, the system collapses.

🚩 Red Flag #6: Fake History and False Regulation Claims

Precise Planning claims it has been around since 2007. A quick WHOIS domain lookup tells a very different story:

Marketing website created: May 2024

Trading platform system launched: August 2024

This is a blatant lie. If they can’t even be honest about their founding date, how can they be trusted with your money?

The Big Picture: Why Precise Planning Is Dangerous

When you connect all these red flags, the picture becomes crystal clear:

The market feed is fake.

The AI is pre-scripted.

No real trades are executed.

Recruitment is mandatory.

Referral rewards come from deposits.

The history is fabricated.

Fees are structured like a Ponzi scheme.

This isn’t a trading platform. It’s a well-disguised scam that uses the language of trading to appear legitimate.

Final Verdict: Scam or Legit?

✅ Legitimate platforms (Binance, Bybit, Kraken):

Transparent APIs and matching engines.

Fees from trades, not deposits.

No activation fees.

No forced recruitment.

Real regulatory licenses.

❌ Precise Planning:

Hard-coded fake data.

AI promises with fixed returns.

Commissions from deposits.

Invite-to-trade structure.

False history and fake regulation.

Conclusion: Precise Planning is a Ponzi scam, not a legitimate trading platform.

Should You Invest?

The answer is simple: No. If you still think you’re making money inside Precise Planning, remember — your profit is someone else’s deposit. The moment new recruitment slows down, withdrawals will be frozen, and the platform will vanish like many others before it.

My Advice

Never trust platforms that promise guaranteed profits.

Always verify if a platform connects to real exchanges and provides transparent data feeds.

Avoid systems that require recruitment or activation fees.

Stick to regulated exchanges where trading activity is verifiable.

What Do You Think?

Now it’s your turn.

Do you believe Precise Planning is legit, or do you agree that it’s just another Ponzi scheme waiting to collapse?

Leave your opinion below — your insight could help protect others from falling into this trap.

Table of Contents

Recently, I received a question about my thoughts on RedShell, which is connected to redshellco.com — a platform that claims to operate a crab fattening and farming business.

The big question:

Is RedShell a legitimate crab farming business or just another investment scam?

Let’s break it down in detail — from how it works, to actual crab fattening economics, sustainability, red flags, and whether it’s a Ponzi scheme disguised as aquaculture.

What is RedShell?

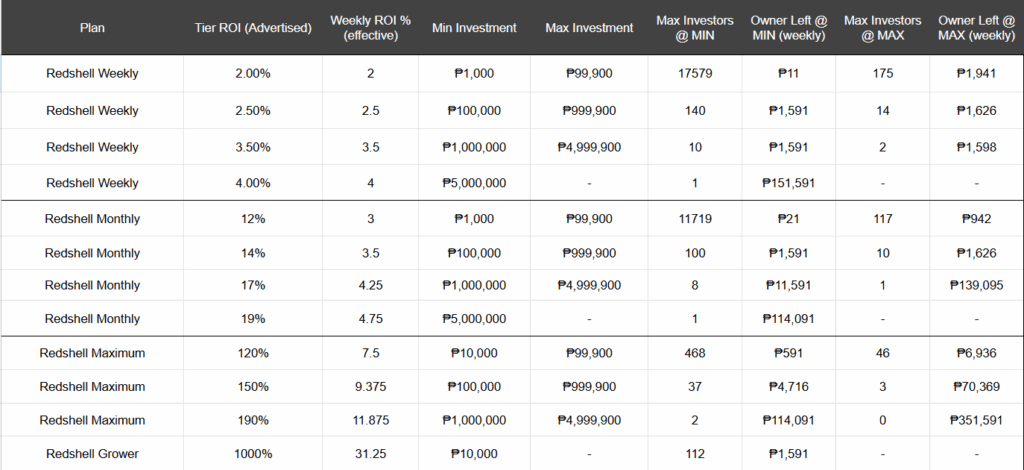

RedShell is an online investment platform that claims to operate a crab farming business and promises investors guaranteed returns from 174% up to 1,000% in just a few months.

They offer multiple investment plans with fixed weekly ROI, and you can also earn through their multi-level referral program.

How Do You Earn in RedShell?

There are two main income sources:

Passive Income from Investment – You put in money, RedShell says they’ll use it to buy “skinny” crabs, fatten them in their farms, then sell at a profit, giving you 2%–4% weekly returns (or higher, depending on the plan).

Referral Commissions – RedShell has a 10-level deep referral system, paying 6% for direct referrals and 0.5% for indirect referrals.

💡 Code Analysis Proof: Based on RedShell’s own backend code, referral bonuses are taken directly from the deposit of your downlines, NOT from actual crab sales. This is a major pyramid scheme indicator.

Is It Sustainable Based on Real Crab Fattening?

To answer that, we need to understand real crab fattening in the Philippines.

📌 How Real Crab Fattening Works

Buying Price of Skinny Crab: ₱350 – ₱450/kg

Fattening Cycle: 15 days for male crabs, ~30 days for female crabs (average 15–20 days)

Selling Price after Fattening: ₱1,000 – ₱2,400/kg depending on market and season

Best Season: “Ber” months & Chinese New Year (high demand, higher prices)

Sample Computation (Real Crab Fattening)

Season / Price Level

Buying Price (₱)

Selling Price (₱)

Profit (₱)

ROI (%) per Cycle

Normal – Low

400

1,000

600

150%

Normal – High

400

2,000

1,600

400%

Peak – Low

400

2,300

1,900

475%

Peak – High

400

2,400

2,000

500%

These are the best possible selling prices under ideal conditions, but not consistent all year round due to market fluctuations, mortality, disease outbreaks, and seasonal demand — and this still does not include production costs or the initial investment required to build and operate a crab farm.

Why RedShell’s Weekly Payout is Unrealistic

In real crab farming:

You cannot harvest and sell every week.

ROI is per 15–20 days (male) or 30 days (female).

Even in peak seasons, consistent weekly payouts are impossible without fresh investor money.

The “No Limit on Investor” Problem

One of the biggest sustainability issues: RedShell has no cap on the number of investors.

Based on actual production capacity from a 1,000-box crab farm, here’s the maximum sustainable investors before payouts exceed actual farm profit:

With no investor cap, once the number of investors exceeds the farm’s real production capacity, the only way to pay old investors is from new investor deposits — the core mechanism of a Ponzi scheme.

Unrealistic Weekly ROI

2% weekly → 171.8% annually.

4% weekly → 610.6% annually.

In real-world crab farming, even in efficient large-scale operations, 42%–66% annual ROI is realistic — nowhere near these figures.

Payout Schedule vs Biological Cycle

Crabs do not fatten in a single week — the minimum cycle is 15 days for males and 30 days for females. If RedShell is paying weekly, it means investors are getting paid before any actual harvest happens.

Referral Commissions Taken from Deposits

Analysis of RedShell’s website code shows that referral payouts come from deposits made by new members, not from crab sales. This is a hallmark of pyramid/Ponzi schemes.

100% Capital Protection Claim

No legitimate agribusiness can guarantee both your full capital and fixed profits. Real crab farming faces mortality risk, disease outbreaks, typhoons, price crashes, and market delays.

Fixed Tiered Income Regardless of Market

In real crab farming:

Prices fluctuate by season.

Mortality rates vary.

Demand changes constantly.

A fixed return of 2%, 4%, 120%, or 1,000% ignores all these realities and is a clear sign it’s not tied to genuine farming operations.

Hypothetical Production Requirements

If one investor puts in ₱100,000 and earns 4% weekly → that’s ₱4,000 in weekly payouts. If there are 100 such investors → ₱400,000 in weekly payouts.

If the profit per kilo is ₱2,000, they would need to sell 200 kilos per week — that’s 10,400 kilos per year. This would require a massive crab farm — which RedShell has not shown evidence of owning or operating.

Red Flags in RedShell

Guaranteed 174%–1,000% ROI → Impossible in real crab farming.

Weekly payouts despite 15–30 day cycles → Paying without harvest.

Unrealistic annual ROI → Far above 42%–66% real-world returns.

Referral commissions from deposits → Ponzi/Pyramid structure.

100% capital protection claim → “Too good to be true” promise.

Fixed income despite market fluctuations → Not possible in genuine aquaculture.

Final Analysis – Scam or Legit?

The crab fattening business appears to be just a front.

Payouts likely come from new investor deposits rather than actual crab sales.

This is a traditional Ponzi scheme with a multi-level marketing twist.

If you’re thinking of investing in RedShell, think twice. Real crab farming can be profitable, but not through guaranteed fixed weekly returns — and definitely not in a scheme that depends on new investor money to pay old ones.

💡 Recommendation: Avoid this investment. If you want to get into crab farming, do it directly and manage your own production, where you control the risks and rewards.

Table of Contents

ADA or Apex Digital Academy is now everywhere on TikTok and Facebook.

It’s quite difficult to find information about this program because most of its details are hidden. You actually have to purchase their online course before you can fully understand what they’re really offering.

This lack of transparency raises questions, so in this review, I will share everything I found out about ADA, based on my own observations and experiences.

What is APEX Digital Academy (ADA)?

Based on videos circulating on TikTok and Facebook, Apex Digital Academy is an online training program that offers digital skills training and opportunities to earn through social media and affiliate marketing.

In short, it’s presented as an online course that will supposedly teach you “legit ways to earn money online.”

According to their official Facebook page, they position themselves as a “One Stop Online Business Solution.”

Inside the ₱990 Entry-Level Course – “The Digital Success Ladder”

When you buy the entry-level course, you get four videos. But here’s the big question:

Do you actually learn something useful?

Video 1 (16 minutes)

This video shows success stories of students who enrolled in the advanced course.

Examples: Some were allegedly interviewed by radio programs, and others claimed to have earned six figures after joining the advanced course.

Observation: For me, this video doesn’t really teach practical skills you can use right away. It felt more like hype-building for the next videos and the advanced program.

Observation: It’s ironic because the video also mentions “Investing in the Wrong Business or Scam Schemes” and asks “Have you been a victim of networking?” – yet ADA’s advanced course is actually tied to a networking-style affiliate system (more on that later).

Video 3 (2 hours 19 minutes)

This video introduces:

Freelancing

E-commerce

Affiliate marketing

Social media monetization

Digital product selling

Observation: This was very basic. You can find the same information for free on YouTube. In fact, many YouTubers teach these topics in detail and for free.

For the ₱990 you spend on ADA’s entry course, you could enroll in a more structured, advanced, and clearer course on platforms like Udemy – often for the same price or cheaper.

Video 4 (1 hour 45 minutes)

This video focuses on:

“The 4 Secrets to Fast Success in Online Business”

Reasons why you should choose ADA over freelancing, e-commerce, other affiliate programs, and digital product selling

Observation: This part was a bit contradictory. In Video 3, they introduced those business models. But in Video 4, they dismiss them as inferior and say ADA is the better option.

It would have been clearer if they had just presented ADA directly instead of spending time introducing other models only to discredit them later.

Analysis of the Entry Course

For me, the real purpose of the four videos is to upsell the advanced course.

You pay ₱990 not to learn real skills but to be funneled into their sales process.

This is what I would describe as a “bait-and-switch” pattern (my opinion based on what I saw):

The ₱990 course was marketed as an online course, but the videos turned out to be mostly introductory, mindset-setting content designed to pitch the ₱69,999 advanced course.

If you don’t upgrade, you won’t get much value.

Real tools and earning potential are locked behind the advanced program.

Other red flags in the entry course:

Minimal practical value: The four videos do not teach actionable skills you can use immediately.

Emotional triggers: They use strong emotional and aspirational marketing to push you to “upgrade.”

The Advanced Mastery Program (₱69,999 – ₱99,999)

If you decide to upgrade, you’ll get access to the Advanced Mastery Program, which includes:

Apex Digital Academy Pathways to Character Excellence

Mentoring session with a multi-millionaire influencer

AI Evolution Summit 2025

The 7-Figure TikTok Affiliate

The Art of Strategic Persuasion

Sell Smart Not Hard

Digital Business Account – web portal where you view commissions

Official ADA affiliate access – you can now earn money by promoting ADA

Digital Dominance – online advertising course

Income Protection

Video Mastery Program

Personal e-wallet

Digital products

Price:

Regular price: ₱99,999

Promo price: ₱69,999

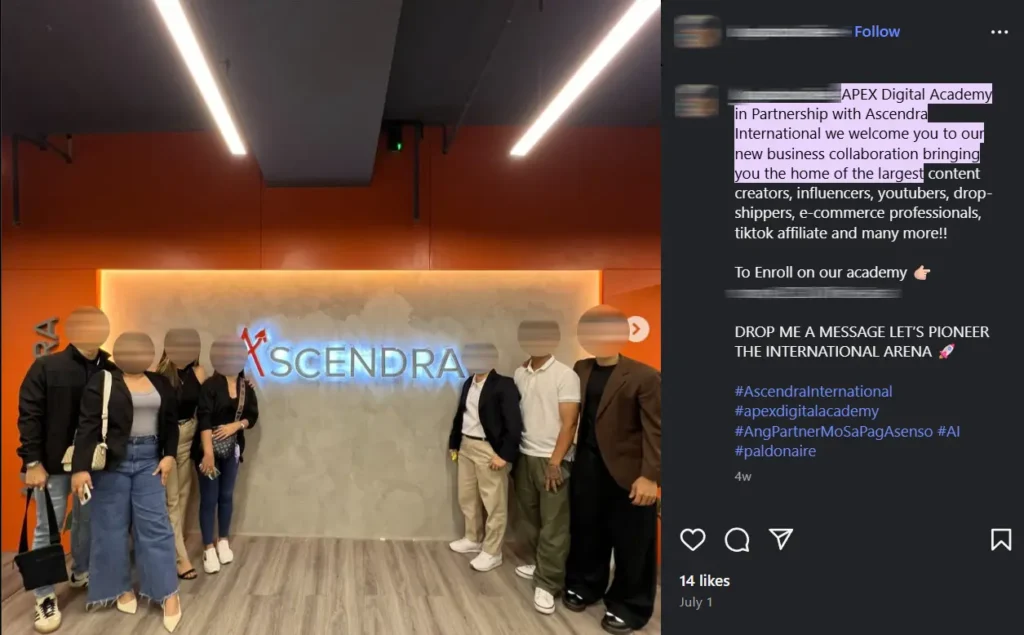

Connection to Ascendra International

Once you join the Advanced Mastery Program, your affiliate dashboard, e-wallet, and “income protection” features are tied to Ascendra International, which is in partnership with ADA.

This partnership was confirmed in a post dated July 1.

Why This is a Red Flag for Me

While ADA advertises itself as a digital skills training program, in the end, it heavily relies on a recruitment system connected to a networking-style structure to generate income.

Here are the major red flags I observed:

Bait-and-switch funnel:

You pay ₱990 for the entry course, but its real purpose is to pitch the ₱69,999 advanced program.

Urgency and scarcity tactics:

Almost every affiliate will tell you “there are only two slots left,” even if that’s not true, to pressure you to pay quickly.

Lack of transparency:

It’s hard to find detailed information about ADA’s structure without buying their courses.

You don’t really know what you’re buying until you’re already inside.

Recruitment focus:

In the end, it feels like a networking system. You expect to build skills, but the income model pushes you to recruit others into the program.

My Final Review of ADA

Based on my experience, I do not recommend APEX Digital Academy.

It is a high-risk program with questionable marketing practices, and the training value is not proportionate to the cost.

There are many other online courses available (like Udemy or Skillshare) that are:

Legitimate Alternatives

1. Udemy

Offers comprehensive courses on affiliate marketing, social media ads, and freelancing for as low as ₱500–₱3,000.

Example: “The Complete Digital Marketing Course – 12 Courses in 1”

2. Skillshare

Subscription model (~₱800/month) gives access to thousands of courses on digital skills.

3. Coursera

Offers certified courses from universities and big companies.

Many courses can be audited for free.

4. YouTube Channels

Creators like Sarah Chrisp and Pat Flynn share free in-depth tutorials on affiliate marketing, Drop shipping and content creation.

What Should You Do Instead?

Avoid ADA if you are not fully aware of the risk and if you’re not prepared to spend a large amount just to get started.

Look for a program that is:

Transparent about what you’re buying

Focused on teaching real skills

Does not rely on recruitment as a primary source of income

Your Turn

What do you think after reading this review?

Do you believe APEX Digital Academy is ethical and worth joining?

Or do you think it’s a program that should be avoided?

Comment your thoughts below. Your feedback can help others decide whether or not to join ADA.

APEX Digital Academy is not recommended. It may seem promising on the surface, but the structure is highly focused on upsells and recruitment rather than real skills training.

If your goal is to genuinely build your skills in freelancing, affiliate marketing, or digital business, you’re better off investing in programs that are affordable, transparent, and skills-based.A? Do you see it as a legitimate program or a high-risk funnel? Share your thoughts in the comments – your insights can help others decide.

Table of Contents

Today, let’s talk about a brand-new application where you can actually earn money just by walking. Yes, you heard that right—simply by walking.

WalkWork is a completely free application where you can convert virtual credits called Step Energy into gift cards like Amazon, Sephora, eBay, or most importantly, convert it directly into real money via PayPal.

It is available for both Android and iOS users, making it very accessible.

What is WalkWork and How Does it Work?

WalkWork is a step-counter rewards app that turns your physical activity into real money. Once you download the app, it tracks your steps automatically. The more steps you take, the more Step Energy you earn.

Traditionally, users had to collect 4,500 or even up to 12,000 Step Energy points before they could withdraw their earnings. This made it difficult for many people to cash out.

But now, WalkWork has released a brand-new feature called Lucky Spin that makes it much easier to earn real money faster.

New Feature: Lucky Spin

The Lucky Spin feature allows you to earn $1.25 instantly once you accumulate the target amount displayed in your Lucky Spin progress bar.

You no longer need to wait until you have thousands of Step Energy points.

You can withdraw immediately after reaching $1.25.

When you first register, you get a free Lucky Spin. However, if you want additional spins, you will need to refer other people to use the application.

There is also a Leaderboard section. If you manage to be in the Top 3, you may get bonus rewards or priority withdrawals.

Ways to Earn Step Energy

If you want to increase your earnings faster, here are the main ways you can collect Step Energy and dollars in WalkWork:

1. Lucky Spin

Each spin can add money directly to your progress bar.

Once you hit $1.25, you can withdraw instantly.

You can spin once for free when you register and gain extra spins through referrals.

You can repeat the Lucky Spin cycle after every withdrawal.

2. Referrals

Invite friends and family to download WalkWork using your unique referral code.

When someone registers with your code, you both receive extra Step Energy (up to 110 Step Energy).

More referrals = more spins + faster earnings.

3. Walking

WalkWork counts your steps every day.

You can earn 100 Step Energy per day for up to 10,000 steps daily.

Make sure to collect Treasure Chests throughout the day because they contain bonus energy points.

4. Daily Logins and Daily Walking Rewards

Log in every day to receive daily bonuses.

These stack on top of your step count, so don’t forget to open the app daily.

5. Bonus Activities and Challenges

Occasionally, WalkWork will release extra challenges or bonus tasks.

Completing them can help you accumulate Step Energy much faster.

Earning Calculation Example

If you consistently walk 10,000 steps every day and maximize your Step Energy from all activities:

You can earn around 100 Step Energy per day.

If you rely only on walking, it might take around 45 days to reach the old payout threshold.

However, with Lucky Spin and other bonus methods, you can now withdraw $1.25 multiple times much faster.

Important Reminders: Avoid Getting Banned

WalkWork has a strict system to prevent abuse. To avoid losing your account or payout, never do the following:

Do not use VPNs or emulators.

This can trigger location mismatches and flag your account.

Do not fake your steps.

Using third-party step generators or spoofing tools can get you permanently banned.

Follow all the rules.

If you are caught cheating, you will not be able to withdraw your earnings.

Is WalkWork Legit or a Scam?

Based on my research and testing:

WalkWork is legit.

Many users, including myself, have successfully withdrawn money from the app.

It is not a scam, but keep in mind that earnings are small and not meant to replace a job.

Use my referral code NZ3EGYL1 or NAKPJ90X to get an extra 110 Step Energy when you sign up.

Once you’ve tried it, comment below:

What do you think about WalkWork?

Do you find it helpful in boosting your physical activity while earning?

Have you successfully withdrawn from the app?

Your experience can help others decide if this app is right for them.

Table of Contents

A new platform called FlickerAlgo has been making waves online, claiming to be an advanced AI trading platform backed by a reputable investment firm.

It promises high profits, server-based trading systems, and "secure cold wallet storage." But is it really legitimate—or just another scam designed to fool investors?

In this review, we’ll break down all of FlickerAlgo’s claims and analyze them with proof.

We will check its licensing, websites, trading operations, referral system, and fund handling. Screenshots and code analysis will also be included to validate each finding.

FlickerAlgo claims to be owned or controlled by Go Invest LLC, a legitimate investment adviser registered with the U.S. Securities and Exchange Commission (SEC). They even display a copy of Go Invest LLC's SEC license to appear regulated.

Fact: This claim is FALSE

The website goinvestllc.com that FlickerAlgo displays as its "parent company" is fake.

WHOIS records show goinvestllc.com was only created in 2025, almost at the same time as flickeralgo.com.

Meanwhile, the real Go Invest LLC domain is goinvest.us, which was registered in 2018 and is consistent with SEC records.

Screenshot: WHOIS comparison of goinvestllc.com vs goinvest.us

Conclusion: FlickerAlgo is misusing the SEC license of the real Go Invest LLC. The two platforms have no real connection.

2. Services Offered vs. SEC-Registered Business

What FlickerAlgo Claims

Data support

Blockchain technology

Investment strategies

Development of trading platforms

Technical guidance

What the Real Go Invest LLC Offers

According to their Form ADV filed with the SEC and their official domain goinvest.us, the legitimate services are:

Retirement plan advisory and IRA rollovers

Investment platform using mutual funds and ETFs

Auto-rebalancing of client portfolios

Financial education

Go Invest LLC SEC Form ADV - listing goinvest.us as the official domain

No mention of crypto, forex, or AI trading exists in any of the official SEC documents.

Conclusion: FlickerAlgo’s advertised services are completely inconsistent with the real business of Go Invest LLC.

3. Trading & AI Bot Analysis

Claim: FlickerAlgo uses AI bots integrated with Binance & OKX

They promote advanced algorithmic trading technology integrated with major exchanges.

Fact: This claim is FAKE

Our analysis of FlickerAlgo’s JavaScript code (from its platform) revealed the following:

Strings like "BINANCE:BTCUSDT" appear in the code, but they are hardcoded for display only.

No API calls to Binance, OKX, or any exchange were found.

The “Live,” “Running,” and “SmartTrade” statuses are purely UI elements, not connected to any backend trading engine.

Conclusion: There is no real trading happening on FlickerAlgo. What you see is scripted front-end display only.

4. Referral System (Pyramid Structure)

FlickerAlgo's referral program rewards users with:

One-time commissions: 30% direct, 20% indirect

Team income: 8%, 6%, 4%, 2%, and 1% from levels 1–5

Why is this a red flag?

Commissions are funded from deposits of new investors, not real trading profits.

This structure fits the classic definition of a pyramid scheme.

5. Cold Wallet & Fund Handling

Claim: Your funds are safe because they are stored in cold wallets

Fact: There is no evidence of real cold wallet storage

FlickerAlgo does not provide any blockchain wallet addresses for verification.

Funds are pooled into central accounts controlled by the operators.

Withdrawals are paid out using deposits from new users—a Ponzi scheme model.

Note: Fake GCash payment authentications have also been reported, making deposits and withdrawals appear legitimate when they are not.

6. JapanIndicator.com & Subsidiary Claims

FlickerAlgo (via goinvestllc.com) claims to be connected to japanindicator.com.

Fact: Connection remains unverified

japanindicator.com and goinvestllc.com are not identical in WHOIS and DNS records, but they do share similar traits:

Both use Cloudflare for hosting and DNS protection.

Both have WHOIS privacy enabled, hiding the true owner’s details.

Differences in WHOIS data:

japanindicator.com was registered on August 20, 2023, via Gname.com Pte. Ltd., with nameservers: jakub.ns.cloudflare.com and cloe.ns.cloudflare.com.

goinvestllc.com was registered on May 25, 2025, via NameSilo, LLC, with nameservers: fred.ns.cloudflare.com andmaya.ns.cloudflare.com.

No direct confirmation from JapanIndicator.com

JapanIndicator.com itself has made no public statement confirming any relationship with goinvestllc.com or FlickerAlgo. All claims of connection originate only from goinvestllc.com’s side.

Conclusion:

While both domains use Cloudflare and WHOIS privacy, they are not identical in registration details. The connection claimed by goinvestllc.com remains unsubstantiated and one-sided, making it likely a tactic to build false credibility.

7. Ponzi Pattern & Phishing History

FlickerAlgo previously operated as fireflyanalysis.com, which was flagged by Google as a phishing site.

After being flagged, they rebranded to FlickerAlgo.

This is a typical tactic used by fraudulent platforms.

8. Server Tiers & Profit Claims

FlickerAlgo has S1–S6 server tiers with varying investment amounts.

Official site:

Lists server fees and investment ranges.

No official profit percentages published.

Marketing materials:

Promoters claim 1.5%–2% daily returns, but these are unverified.

Code analysis:

No logic exists for real profit calculation.

All numbers are scripted and displayed via the UI.