Have you heard of Tier One Online Services (tierone.to)? Some people are asking whether it’s a trusted trading platform or if it’s just another scheme like Aurora, which turned out to be nothing more than a Ponzi disguised as an investment opportunity.

In this blog, let’s dig deeper. We’ll break down how Tier One actually works, what it promises, and why its system is not sustainable despite the bold claims.

According to the platform itself, Tier One promotes itself as the “number one trading platform” — long-term, trusted, and allegedly a legitimate passive income opportunity.

The big question is:

Before answering, let’s examine how people supposedly earn money inside Tier One.

Tier One offers two main investment plans:

That’s not all. Tier One also pays out commissions for recruiting new members:

On top of this, they introduced credits:

At first glance, the system looks attractive: quick profits, referral bonuses, and even consumer products. But this raises the critical question:

Where does the company actually earn the money to pay investors?

Tier One claims that their profits come from cryptocurrency trading. On their website, you’ll even find screenshots of supposed trade profits, often showing millions of pesos earned from Ethereum futures.

But are these claims legitimate? Are these screenshots reliable proof that Tier One is really earning through trading?

The short answer is: No.

After investigating the platform, it’s clear that Tier One Online Services operates as a Ponzi scheme. None of the so-called profits come from legitimate trading. Instead, all payouts — whether from plans, recruitment commissions, or credits — come from the money deposited by new investors.

Here are the major red flags:

The trading screenshots shown on Tier One’s site are not proof of real trading activity. Anyone can fabricate or edit screenshots from demo accounts, Excel sheets, or PDFs.

Real proof of trading requires verifiable, third-party-verified records such as:

These records show actual trades, profits, and losses. Without this, screenshots are meaningless. If Tier One truly trades, they should be able to connect their broker account to a transparent, real-time tracking service. The fact that they haven’t is a huge red flag.

This level of return is mathematically impossible to sustain in real trading.

Let’s use compounding math:

Now imagine thousands of investors doing the same. The total money owed would exceed the entire market capitalization of cryptocurrencies. This is why such returns are impossible in reality.

Since no legitimate trading proof exists, the only source of payout is money from new recruits. This is the core definition of a Ponzi scheme.

The system only lasts as long as new money keeps coming in. Once withdrawals exceed deposits, the entire scheme collapses.

This is why early participants sometimes boast that they “made money” — but when the platform shuts down, they disappear silently, leaving later investors with nothing.

Some investors claim they “earn daily.” But here’s the truth:

As long as there are new investors, withdrawals are processed. But once the inflow slows down, withdrawals are delayed or denied. This is a classic Ponzi tactic: keep balances growing on-screen to trick investors into believing the system is real.

If Tier One truly had a trading strategy that guaranteed 20% to 50% returns within days, why would they need investors at all?

Think about it:

The fact that they’re aggressively recruiting investors proves that their real income comes from deposits, not trading.

To summarize, Tier One is unsustainable for several reasons:

This mismatch between their claims (“we earn from trading”) and reality (“we rely on new deposits”) guarantees that the system will collapse — it’s only a matter of time.

Tier One, just like Aurora and Netflex before it, is a Ponzi scheme disguised as a trading investment platform. It hides behind fancy words like “trading” and “passive income,” but the mechanics are the same:

The absence of market risk — replaced with “guaranteed profit” — is itself a giant red flag. Real investments always carry risk. When someone removes risk and promises fixed profit, it’s no longer investing, it’s scamming.

🚨 My advice: Avoid Tier One. Do not invest. And definitely do not promote it to others. Doing so only feeds the cycle and hurts more people in the end.

Now I’d like to hear from you: What’s your opinion on Tier One? Do you think it’s legit or just another Ponzi in disguise? Share your thoughts in the comments below.

Promise on the table: “450% income after 3 days, 15% reinvest bonus, and 10% deposit bonus.”

That’s what AuroraPhil is currently advertising to would-be investors.

Domain: auroraphil.com • www.auroraphil.com

You’re probably asking: can real trading deliver percentages like that?

Let’s examine everything—exactly and completely—based on what the site and its promoters show publicly, what users report in open groups, what can be inferred from the domain/ownership signals, and what we can verify (or fail to verify) from their “proof of trading.”

AuroraPhil is an investment website spreading through Facebook groups via referral links (the URLs typically include a parameter like AURORAREFER=...).

The pitch revolves around fixed-term packages where you “invest” into a plan and receive a pre-declared return after a short period.

The headline claim they push most aggressively is the “coin Holder Package” promising 450% in just 3 days, plus a 15% reinvest bonus and 10% deposit bonus.

They also float other packages such as 290% in 5 days (with 12% reinvest + 10% deposit bonus), and, in different materials, 25% in 6 days and 90% in 16 days (some posts even show 9% in 16 days—the inconsistency is itself noteworthy). A “SUPER VIP ACCESS” tier is also mentioned, implying extra benefits if you put in more money.

How it’s framed: deposit → wait the stated days → withdraw your “profit” → optionally refer others to boost earnings.

This is the classic HYIP (high-yield investment program) workflow where the returns are fixed and schedule-based, not variable the way real market-driven trading results fluctuate.

Important identity note: We found no claim from auroraphil.com or its promoters that they are affiliated with Aurora (O.A.) Philippines, Inc. (the furniture company at auroraphils.com). The two appear unrelated, and the investment site does not publicly present itself as connected to the furniture business.

In videos and posts, a person presented as the CEO goes live to show that they “trade” on an exchange (most often named as Bybit) as a form of transparency. Two realities collide with this pitch:

From their livestreams and screenshots, multiple concrete signs indicate a mocked or fabricated trading interface, not a live exchange account:

$79,749.40) with no Bid/Ask, no Index/Mark variants.Bottom line: What’s shown is best explained as a demo/mockup built to impress non-traders, not evidence of actual, externally verifiable trading.

AuroraPhil leans hard on recruitment. Aside from package returns, the materials describe a multi-level referral payout:

This pyramid-shaped structure pays out from incoming deposits rather than from a real, external product or service, which is characteristic of Ponzi economics: earlier participants are paid using money from later participants.

They reference or imply a coin/token, but no transparent proof is provided. To establish a real token, a project should present on-chain facts:

AuroraPhil’s dashboard-only balances (if any) are not evidence of a live token. Without contract addresses, listings, and on-chain activity, the “coin” reads as a narrative layer rather than a real asset.

/auth/register?AURORAREFER=...).From a newcomer’s perspective, two things feel attractive: easy onboarding (email + referral) and pre-declared payouts (you “know” the number on paper).

Unfortunately, those are precisely the two levers HYIPs use to accelerate deposits before people complete due diligence.

Classification: Not Safe.

AuroraPhil (auroraphil.com) fits the risk profile of a Ponzi-style HYIP: extreme fixed returns, referral-centric growth, mocked trading proof, opaque domain/ownership, no audit or custody, and regulatory exposure. The prudent course is to avoid depositing funds and avoid recruiting others.

Bottom line: Given the totality of signals, AuroraPhil is Not Safe.

Scope & method. I’m basing this breakdown entirely on materials I captured directly: front-end code bundles, on-page text, and Network/XHR logs. I’m not leaning on outside marketing blurbs or hearsay. Instead, I’ll walk you through Orbion using its own words and behavior—UI states, API calls, and just as importantly, what’s missing (wallet-connect, signature prompts, on-chain transactions, DEX integrations). The aim is straightforward evidence and clear reasoning—no hype, no dramatics.

Orbion (domain name: orbion.vip) presents itself as an “Advanced DEX Sniping Bot” for the Solana ecosystem. Across the interface copy and feature panels, the product introduces a familiar story:

If you stop here, Orbion looks like a slick, consumer-friendly gateway to “hands-free” Solana trading.

Before we audit Orbion, here’s the minimum a genuine Solana-native trading/sniping tool must demonstrate:

window.solana and wallet-adapter patterns.sendTransaction, TransactionInstruction, or VersionedTransaction.Keep those five pillars in mind. They’re the difference between blockchain trading and a website that simulates balances.

window.solana) or wallet/tx primitives (sendTransaction, TransactionInstruction, VersionedTransaction).Why this matters: Without wallet connect, the app cannot request signatures or touch your on-chain assets. Whatever “trading” it claims to do, it is not being done by you, under your custody, on your wallet.

Why this matters: Without a signature request and a public tx hash, there is no on-chain audit trail. The app can claim “trades,” but users have no verifiable record.

Why this matters: Without DEX interactions, sniping is a branding claim, not a function.

All monetary operations—deposit, withdraw, wallet, dashboard, transactions, investment, subscription, referral commissions—are implemented as HTTP calls to /api/... endpoints. Representative examples include:

/api/wallet/deposit

/api/wallet/withdraw

/api/wallet

/api/transactions

/api/investment

/api/subscription

/api/subscription/active

/api/referrals/commissions

/api/dashboard

And the user profile payload clearly models an internal wallet with database-backed balance and transaction list:

"wallet": { "balance": "0.00" },

"transactions": []

Why this matters: This is custodial and off-chain. You are crediting a balance on a database, not moving funds on Solana. The operator controls the ledger and can mint or revoke balances at will.

The deposit flow is telling:

toDataURL("image/jpeg", 0.8) pattern) and uploads it to the server through an endpoint such as:POST /api/deposit-request

TRC20:..., Solana:...) to display send-to instructions, consistent with manual transfers, not wallet-connected on-chain flows.Why this matters: In Web3, your signature + the resulting hash is the proof. Screenshots are not proof; they’re support attachments in centralized systems. A genuine Solana app would never ask you to upload a payment receipt image to get credited.

Why this matters: The “bot” is a page section that reflects database state, not a live, on-chain trading process.

The interface explicitly promotes fixed daily returns (e.g., “Fixed daily returns on your investment,” “Daily Profit” displayed as 2% in the captured DOM). Elsewhere in the UI text, you’ll find lines like “Up to 2%/3% daily profit potential.”

Why this matters: Fixed daily ROI does not exist in real, market-risk trading. Markets are variable. Any “bot” promising fixed daily yields is not describing normal trading—this is the hallmark of a HYIP (high-yield investment program) structure.

The interface promotes a 1% daily referral commission and exposes a dedicated API to fetch referral commissions:

GET /api/referrals/commissions

Why this matters: A daily, percent-based referral payout tied to “investment balances” is a strong indicator of a pyramid/Ponzi dynamic, especially in the absence of real on-chain PnL to fund it. Legit affiliate programs pay from real product/service revenue or fees, not from new deposits.

Why this matters: Money-handling software should not present itself to the public on a dev-preview rail. For a tool that expects deposits, this is a red flag about release maturity and operational discipline.

Let’s compare Orbion’s claims with its observable behavior:

| Claim | What You Should See in a Real Solana App | What Orbion’s Materials Show |

|---|---|---|

| “DEX sniping bot (Solana)” | Wallet connect; tx signatures; explorer hashes; DEX program IDs | No wallet connect; no signatures; no hashes; no DEX calls |

| “Automated bot” | Live positions, program interactions, AMM routes | UI shell + server-fetched lists; no on-chain evidence |

| “Profit sharing / copy trading” | Profit share on actual PnL from your wallet/account | Upfront “investment,” daily fixed returns, referral overlay |

| “Wallet balance” | Your wallet’s ATA balances mirrored in UI | A platform “wallet” (database balance), not on-chain |

| “Deposit” | Wallet signature or regulated fiat gateway | Manual send + screenshot upload to be credited |

The discrepancy is not subtle. The entire money model is centralized and API-driven, while the entire Web3 layer (connect, sign, verify) is missing.

Taking all of the above together:

Classification:

This fits a centralized HYIP/Ponzi-style investment scheme with a sniping/trading bot veneer. It is not a Solana-native trading/sniping product. It operates off-chain, under operator custody, and simulates yield via server-side balances and referral overlays.

If you’re technically inclined, you can replicate the core findings without any special tools:

/api/wallet/deposit and a /api/deposit-request upload with an image/screenshot.My analysis, constrained to the artifacts you provided, is unequivocal:

Classification: High-risk HYIP / Ponzi-style scheme masked as a “Solana trading/sniping bot.”

Recommendation: Do not treat this as a Web3 product; do not deposit funds you cannot afford to lose; do not promote it as an on-chain trading tool.

If you are assessing platforms in this space, use the five-pillar baseline (wallet connect, signatures, hashes, DEX interactions, wallet balances) to screen for authenticity.

Healthy skepticism isn’t cynicism—it’s due diligence. If a “bot” can’t connect to your wallet, can’t ask for a signature, can’t show a tx hash, and can’t name the DEX routes it uses, it’s not a blockchain trading tool. It’s a website that moves numbers in a database.

Surveyon is one of the more well-known online survey platforms available in Asia, including the Philippines.

Many people are curious if it’s really worth the time, whether the surveys pay fairly, and most importantly—if it’s actually legit or just another scam.

In this blog, I will give you a complete and detailed review of Surveyon based not only on my own script and experience but also with additional research and analysis.

You’ll learn what Surveyon is, how to earn points, what the features are, the pros and cons, potential red flags, and my final verdict on whether it’s truly legit.

Surveyon is a legit online survey panel and mobile application operated by dataSpring, Inc., a global market research company under the INTAGE Group.

The app allows users to answer market research surveys and earn points that can later be redeemed via PayPal or gift vouchers.

Unlike shady apps that make unrealistic promises, Surveyon has been operating for years across Asia, with offices in Tokyo, Seoul, Shanghai, Singapore, Los Angeles, London, and Manila, Philippines.

The company behind it is established in the research industry, which is a positive sign.

Surveyon offers several ways to collect points:

So yes—you can earn money, but the actual value per survey is low. Most surveys give 200–1,000 points, which means you’ll need to complete anywhere from 10 to 50 surveys just to reach $1.

✅ Legit and safe – Backed by dataSpring, a real research company.

✅ Free to join – No need to pay or invest.

✅ Low threshold – You can cash out from $1–$2.

✅ Fast payouts (sometimes as quick as 3 days).

✅ Daily availability – Check-ins and quickpolls provide steady small points.

✅ Consolation points when screened out of surveys.

❌ Low earnings – Surveys pay little; you need dozens to reach even $1.

❌ Survey disqualification – If your answers are inconsistent, you may get fewer invites.

❌ Mixed reviews – Google Play rating is 3.9★; Trustpilot shows 2.5★. Some users complain about account suspension or missing rewards.

❌ Country-dependent availability – More surveys in some countries, fewer in others.

❌ Not sustainable as income – This is clearly a micro-earning app, not a job.

These are not outright scams but things you should watch out for.

Based on my review and all the information I gathered:

Final Verdict: ✅ Legit and Safe

Yes, Surveyon is legit and safe to use. It won’t scam you, and it really pays out, but don’t expect significant money. Use it only for small extra earnings, not as a main source of income.

Surveyon is an honest survey app that really pays, but only at a very low rate. If you want to try it out, you can register for free, use daily check-ins and quickpolls, and redeem via PayPal once you reach the threshold.

But here’s the truth: If you are looking for serious money, this isn’t for you. If you’re happy with small rewards, then Surveyon can be worth your time.

Now I want to ask you: Have you used Surveyon? Did you earn anything from it? Share your experience in the comments—I’d love to know what you think!

This analysis is grounded in first-party technical artifacts originating from the platform itself:

Earlier contextual notes we discussed (e.g., social/WHOIS chatter) are kept to a minimum; the core of this review is the code and the live network traffic produced by the application itself.

The running app is a single-page application (SPA) with a broad feature surface:

The SPA is built with Vue + component libraries (you’ll see Element/Ant patterns in the DOM), and a canvas-based K-line chart renders OHLC candles and volume.

On boot, the SPA fetches a remote JSON configuration that declares:

A representative API line returned by this config is:

https://epi.nz558.com

The front end then binds all REST calls under a common prefix:

/forerest

and proceeds to query:

POST /forerest/kline/find),/forerest/spots/...),/forerest/second/...),Why this matters: the app does not directly call Binance/OKX/Coinbase/CoinGecko/Chainlink/Pyth from the browser. It gets all market data and executes all orders via its own API line. This is the foundation of the “closed-loop” conclusion later.

The line JSON is hosted on OSS (Aliyun) and can be swapped at will. That enables the operator to:

Operationally, this is a hallmark of systems that want flexible domain usage. On its own, it’s not “proof of wrongdoing,” but in combination with the next sections, it becomes a significant risk indicator.

The SPA includes a K-line helper that posts to /forerest/kline/find:

const BASE = "/forerest";

function getKline(payload) {

return http({

url: `${BASE}/kline/find`,

method: "POST",

data: payload

});

}

Real captured responses for the market list/tickers show payloads like:

{

"code": 200,

"data": [

{

"symbol": "BTC/USDT",

"open": 111502.01,

"close": 111244,

"high": 111583.13,

"low": 111226.87,

"chg": -0.0002,

"klineType": 1

},

{

"symbol": "TRX/USDT",

"open": 0.3442,

"close": 0.3440,

"high": 0.3442,

"low": 0.3440,

"chg": -0.0032,

"klineType": 1

}

]

}

Critical implication: whatever prices you see in the chart come from their server. There is no front-end connection to public exchange feeds. If they choose to differ from public marks, the UI will still display their price.

/forerest/spots/...)All Spot actions in the UI call in-house endpoints:

const SPOTS = "/forerest/spots";

function addOrderSpots(body) {

return http({ url: `${SPOTS}/order/add`, method: "POST", data: body });

}

function getOrderPage(body) {

return http({ url: `${SPOTS}/order/page`, method: "POST", data: body });

}

function cancelOrder(body) {

return http({ url: `${SPOTS}/order/cancel`, method: "POST", data: body });

}

function getSpotsBalance(params) {

return http({ url: `${SPOTS}/wallet/balance`, method: "GET", params });

}

UI forms (as seen in your DOM capture) implement:

What you don’t see: a front-end call sending the order to a public venue. Everything is posted to their /forerest/spots/... endpoints.

/forerest/second/...)The seconds/binary module exposes a complete mini-lifecycle:

const SECONDS = "/forerest/second";

function getCycles() {

return http({ url: `${SECONDS}/cycle/findAll`, method: "GET" });

}

function addSecondsOrder(body) {

return http({ url: `${SECONDS}/order/add`, method: "POST", data: body });

}

function getSecondsOrderPage(body) {

return http({ url: `${SECONDS}/order/findPage`, method: "POST", data: body });

}

Risk characteristics of “Seconds”:

The SPA initializes Socket.IO against the active host. There is no wss://stream.binance.com/... or similar in the front-end. This means:

The UI language is USDT-heavy, yet the front-end lacks:

You do see generic phrases like “Third-party Withdraw”, “USD Withdrawal”, “Withdrawal Fee”, “Binding Withdrawal Address.” But the necessary scaffolding a real on-chain flow uses (TXIDs, chain labels, explorer links) is not present in the UI.

Why this matters: even if payouts occur “behind the scenes,” production UIs typically reserve placeholders for TXID/Explorer so that a user can verify a transfer cryptographically. The absence of these hooks strongly suggests a ledger-only model where credits/debits are updated internally without public proofs.

The current interface uses “Staking” wording, but the codebase still contains a Cloud Mining module with endpoints like:

GET /forerest/cloudmining/confInfoPOST /forerest/cloudmining/order/buyPOST /forerest/cloudmining/findPagePOST /forerest/cloudmining/order/findPagePOST /forerest/cloudmining/income/findPageThis is textbook white-label behavior: toggle product names/skins while keeping the same deposit-driven yield scaffolding. Again, there are no on-chain proof hooks on the front-end to validate “earnings.”

Strings and components indicate:

In regulated contexts, referral tooling is usually ancillary. Here, the referral/agent layer is central, tied to deposits and “activity” modules (lotteries, bonus events). This aligns with high-risk monetization patterns.

The production copy includes an explicit “100% deposit guarantee” and “compliant digital asset trading license.”

Bottom line: a high-impact claim with no discoverable evidence in the product is a major red flag.

Within the production copy, blocks referencing other exchange brands appear. In a properly maintained and regulated production build, unrelated brand copy should never ship. Mixed branding is one of the clearest fingerprints of a recycled/white-label codebase deployed under different skins.

addEventListener("contextmenu", ...) with preventDefault() calls).localhost, generic BaseURL placeholders) appear in a production build.BetButton show through in trading buttons.None of these alone proves fraud; together with the closed data/exec pipeline and the product mix, they depict a stack that does not prioritize transparency.

Your DOM snippet shows:

id="k-line-chart") with layered <canvas> elements,BetButton.This proves that the UI indeed renders a familiar exchange-like surface. Paired with the code and network behavior above, we can say with confidence: the surface is exchange-like, but the data and orders are closed-loop.

All browser-side evidence points to “in-house”:

/forerest/kline/find (their server) for chart data./forerest/spots/... and /forerest/second/... (their server) for placement, listing, and cancellation.Translation: prices and settlements are whatever their backend says. You cannot independently verify a trade/fill/settlement against a public orderbook or a published mark index, especially critical for “Seconds” where a single tick flips the outcome.

POST /forerest/kline/find to the active line host (e.g., https://epi...). You will not see public exchange API calls.Each item would be concerning; together they justify a do-not-deposit stance.

From a technical and risk-control perspective, this platform does not meet the bar for a legitimate exchange:

Final stance: Treat Opalp.com as high-risk / behave-as-scam.

Recommendation: Do not deposit. If already exposed, try a small, immediate withdrawal and insist on TXIDs. Escalate if they cannot or will not provide verifiable on-chain proofs.

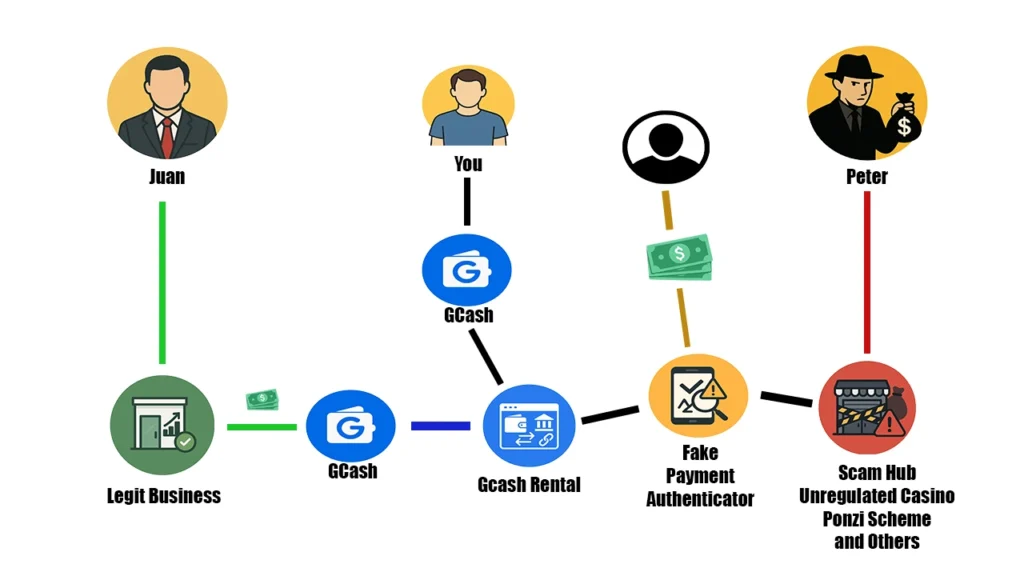

Let’s talk about this new so-called online earning opportunity that has been circulating lately — GCash Rental, sometimes also marketed as Self Rental.

For those who still don’t have any idea what this is, let’s break it down:

GCash Rental refers to the act of “renting out” or “allowing someone else to use” your GCash account through third-party platforms like HDPay in exchange for daily profits.

The idea is simple:

At first glance, it looks like passive income: you don’t need to do anything — just put money in your GCash account, connect it to HDPay or similar apps, and wait for your money to “grow.”

It depends on the rate set by the platform. Most of these sites advertise 1% to 2% daily return.

It sounds attractive, especially to those looking for “easy money.” But before you get tempted, the important question is:

Is this legal?

The income you see from GCash Rental does not come from legitimate sources. It is connected to illegal activities and is part of a Money Laundering Scheme.

Let’s use an example:

Peter needs Juan’s help to move money, but here’s the problem: If Juan and Peter transact directly, they will get flagged under AMLA (Anti-Money Laundering Act). It will be traceable, and both could be charged.

So, what do they do?

They use a third-party layer — this is where GCash Rental platforms come in.

You, the ordinary user, get lured in by the promise of 1% to 2% daily passive income.

This Fake Payment Authenticator is used by:

When people send money to these illegal hubs, the funds are funneled into your GCash account (alongside hundreds of other rented accounts). But the money doesn’t stay with you.

By the time it reaches Juan, the money looks clean — even though it came from scams.

The process perfectly fits the Money Laundering Cycle:

You are essentially serving as a money mule — a bridge for illegal money to move.

Some people ask: “Isn’t there at least one GCash Rental platform that’s legal?”

The answer: None. Zero.

Here’s why:

Many people who tried GCash Rental ended up with:

If you really want to earn with GCash, use regulated features like:

These are all BSP-regulated and legal.

There is no such thing as a legitimate GCash Rental. Every platform offering it is part of an illegal network tied to scams, unregulated gambling, and fraud.

The promise of 1% to 2% daily return is the bait.

The reality: you risk losing your money, your account, your reputation, and your freedom.

So ask yourself:

The wise answer is simple: Stay away. Don’t rent your GCash. Don’t be a money mule.

Drop your opinion in the comments — let’s spread awareness so fewer people fall into this scam ecosystem.

Today, we are going to take a deep dive into a platform that has been making rounds online, especially here in the Philippines. Its name? DUOB TOP.

Here are the domains connected to DUOB TOP:

The big question is: Is DUOB TOP a legitimate and honorable way to earn money online, or is it simply another elaborate scam waiting to collapse?

Let’s answer that question thoroughly, step by step.

According to its official website and marketing materials, DUOB TOP claims to be an AI-driven GameFi platform.

The central idea they are trying to sell is that their platform’s main “products” are so-called game equipment or game props. They want users to believe that these props are traded as GameFi assets, similar to NFTs, characters, skins, virtual lands, or special items used in various games.

The platform even throws around the names of popular titles such as GTA, Dota 2, World of Warcraft, and Genshin Impact to make their business sound connected to legitimate gaming ecosystems. The claim is that DUOB TOP sources these digital items, trades them internationally, and then distributes profits back to investors.

But the question is: Is any of this actually true?

The answer, unfortunately, is no.

All of these so-called “game props” that DUOB TOP showcases on its website and in its app are nothing more than a front. They are unrelated to how the platform actually generates money for its members. In fact, they are fake, non-functional items designed solely to give an illusion of legitimacy.

In other words, the game items being displayed are fake digital assets with zero value.

The games themselves—GTA, Dota 2, WoW, Genshin—have no partnerships or integrations with DUOB TOP. The platform merely invokes these names to appear credible.

This is the critical question.

If the so-called “game items” are fake, then where does the profit promised to investors actually come from?

The reality is: All of the profit being distributed in DUOB TOP comes directly from the deposits of new investors.

The platform is not generating income from any real product or service. It is simply moving money around. Early investors get paid with the money from newer investors, while the platform operators and recruiters skim their share off the top.

This structure is the classic definition of a Ponzi scheme.

Over the course of my investigation, I found several red flags that reinforce the conclusion that DUOB TOP is a scam. Let’s go through them one by one.

DUOB TOP claims you can earn up to 135% profit in just 30 days.

If you do the math, these figures are astronomical and completely unrealistic in any legitimate financial market.

No real business, no stock market, no crypto trading bot, and no GameFi project can guarantee such daily profits consistently. These are classic Ponzi promises designed to lure in greed-driven investors.

Another immediate warning sign is their marketing language.

They boldly declare that DUOB TOP investments are “No Risk” and provide “100% fund security.”

This alone is a dead giveaway of a scam.

Why? Because no legitimate financial or investment platform in the world can guarantee zero risk. The moment you see a company promising no risk and guaranteed profits, you should automatically assume it’s fraudulent.

DUOB TOP heavily emphasizes recruitment. Their compensation plan rewards you with:

This is not a standard affiliate marketing model. In legitimate affiliate programs, commissions are tied to the sale of actual products or services.

In DUOB TOP, commissions are tied only to deposits made by new members.

That makes it a pyramid scheme, which is inherently unsustainable. The system only works as long as there are endless new recruits continuously putting in money. Once recruitment slows down, the entire scheme collapses.

Inside the platform’s app, you will see flashy tabs labeled “Contest,” “Game Props,” and “Trade.”

All of these are decorations to make the app look sophisticated, when in reality they have nothing to do with how money is moving inside the system.

DUOB TOP proudly showcases certificates such as a Colorado business registration and an MSB printout from the U.S. Treasury’s FinCEN website.

Here’s the truth:

Therefore, their displayed licenses are misleading props—not proof of legitimacy.

Upon analyzing DUOB TOP’s code, it became clear that the platform is built on a white-label template.

uunn.org), revealing that it was not built uniquely for DUOB.This contradicts their marketing story of having a sophisticated proprietary AI trading system.

To push the scheme, DUOB TOP incentivizes recruiters:

On top of these small recruitment bonuses, DUOB TOP also promotes what they call a “Team Development Monthly Salary.”

At first glance, it looks like a structured job compensation plan with salary levels, but in reality, it is simply another way to push members into nonstop recruiting.

The so-called salary is based entirely on the size of your team and the deposits made by those recruits:

While these numbers may look attractive, the “salary” is not backed by any real product or legitimate service.

It is completely dependent on constantly recruiting new members and ensuring they deposit money into the platform.

In short, it’s a fake job structure—a pyramid scheme disguised as a career path, designed to keep people chasing bigger teams instead of recognizing that the entire system has no genuine source of income.

But again, all of this income is funded only by new deposits. There is no real product generating profit.

DUOB TOP is sustained only as long as new investors keep joining. The moment recruitment slows down, the system will no longer have enough incoming funds to pay out profits.

When that happens, the operators will simply shut down the website, disappear with the money, and leave thousands of members with heavy losses.

This is the destiny of all Ponzi and pyramid schemes, and DUOB TOP is no different.

The verdict is clear: DUOB TOP is not safe.

It is a Ponzi scheme disguised as a GameFi platform. It offers no real products, no real services, and no genuine connection to the gaming industry. It survives only by recycling new deposits into fake profits.

Sooner or later, this platform will collapse, and investors will lose their money.

My advice: Do not invest. Do not promote it. Do not recruit others into it.

What do you think about DUOB TOP?

Leave your thoughts in the comments below. Share your experience so that others can learn from it. By speaking out, you can help prevent more people from falling victim to this Ponzi scheme.

📌 Final Word: Always remember, when a platform promises high returns with no risk, guaranteed profits, and commissions based only on recruitment—it is not an opportunity, it is a trap.

In the world of online trading, hundreds of platforms promise life-changing profits, smart AI strategies, and “guaranteed returns.” Unfortunately, most of them vanish overnight, leaving investors with nothing but frustration and loss.

Today, let’s talk about one of the most talked-about names circulating in forums and social media recently — Precise Planning.

If you take a closer look, you’ll see that this so-called platform isn’t just operating from a single website. Instead, it relies on a network of interconnected domains and servers that make up its entire trading ecosystem.

The core URLs tied to Precise Planning include:

On top of that, they also operate front-end portals for users:

All of these domains are tightly connected and controlled by the same operators. Instead of drawing data from the real crypto market, every feed and chart inside these sites is hard-coded and manipulated to create the illusion of genuine trading activity.

Many people ask:

👉 Is Precise Planning a legitimate trading platform?

👉 Or is it just another well-designed scam disguised as a trading opportunity?

Let’s break this down step by step and uncover what’s really happening behind the curtain.

According to its official marketing website, Precise Planning claims to be a regulated global trading platform that was founded in 2007. At first glance, that statement looks impressive — over a decade in the industry, supposedly regulated, and positioned as an established leader.

But is this true? Does Precise Planning really have that kind of history, infrastructure, and transparency?

Spoiler: The answer is no.

Let’s go deeper and examine the red flags that clearly indicate why Precise Planning is not only fake, but also a Ponzi scheme in disguise.

I personally classify Precise Planning as a fake trading system and a Ponzi-style scam. Here are the critical reasons why:

In real trading platforms like Binance or Bybit, the price feeds, order books, and trade executions are live and transparent. They are directly connected to actual markets. Anyone can verify these feeds through APIs or third-party tools like TradingView, CoinGecko, or CoinMarketCap.

But in Precise Planning, everything is hard-coded. The price charts, candlesticks, trade signals, and “market movement” are all synthetic simulations generated by their own servers.

Here’s how it works:

For example, the price of BTC/USDT in Binance may be $60,000. Precise Planning could delay the data by 2 minutes, feed you a signal “Buy Now,” and when you look at the delayed chart inside their platform, it aligns perfectly. This makes you believe the strategy works, when in reality it’s all pre-scripted manipulation.

This is the biggest sign of fakery — there is no transparent, verifiable matching engine or live market connection.

Precise Planning proudly promotes its “AI Smart Trading” and different investment plans. The bigger your deposit, the higher the fixed percentage they promise you — sometimes 30% to 60% returns.

Why is this a problem?

Bottom line: Their so-called AI is just a smokescreen to justify their Ponzi structure.

Looking deeper into the platform code, there is no genuine market execution happening:

What you see on screen are fake trades designed to trick you into believing you’re participating in the market. In reality, your money is just circulating within the platform’s internal system.

Legitimate trading platforms allow you to trade immediately after registration and funding your account.

Precise Planning, however, uses an invite-to-trade system:

This is a classic Ponzi model. Real trading has nothing to do with recruitment. If a so-called platform forces you to recruit to gain access, it’s not trading — it’s multi-level scamming.

In Binance or any regulated exchange, referral commissions come from trading fees your referrals pay when they make real trades.

But in Precise Planning, commissions are taken from the deposits of new recruits. Worse, they allow commissions to flow up to multiple levels, forming a pyramid scheme.

This proves there’s no real revenue model except new money funding old participants. Once recruitment slows down, the system collapses.

Precise Planning claims it has been around since 2007. A quick WHOIS domain lookup tells a very different story:

This is a blatant lie. If they can’t even be honest about their founding date, how can they be trusted with your money?

When you connect all these red flags, the picture becomes crystal clear:

This isn’t a trading platform. It’s a well-disguised scam that uses the language of trading to appear legitimate.

✅ Legitimate platforms (Binance, Bybit, Kraken):

❌ Precise Planning:

Conclusion: Precise Planning is a Ponzi scam, not a legitimate trading platform.

The answer is simple: No.

If you still think you’re making money inside Precise Planning, remember — your profit is someone else’s deposit. The moment new recruitment slows down, withdrawals will be frozen, and the platform will vanish like many others before it.

Now it’s your turn.

Do you believe Precise Planning is legit, or do you agree that it’s just another Ponzi scheme waiting to collapse?

Leave your opinion below — your insight could help protect others from falling into this trap.

Recently, I received a question about my thoughts on RedShell, which is connected to redshellco.com — a platform that claims to operate a crab fattening and farming business.

The big question:

Is RedShell a legitimate crab farming business or just another investment scam?

Let’s break it down in detail — from how it works, to actual crab fattening economics, sustainability, red flags, and whether it’s a Ponzi scheme disguised as aquaculture.

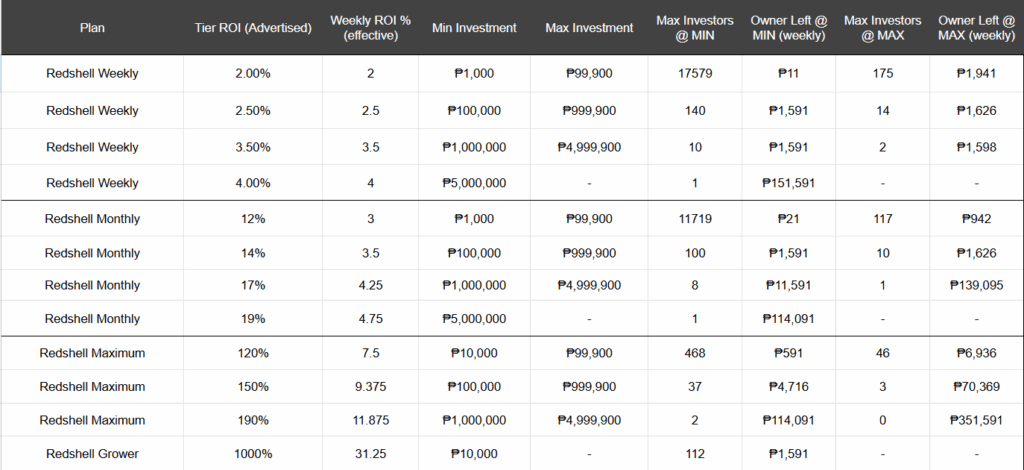

RedShell is an online investment platform that claims to operate a crab farming business and promises investors guaranteed returns from 174% up to 1,000% in just a few months.

They offer multiple investment plans with fixed weekly ROI, and you can also earn through their multi-level referral program.

There are two main income sources:

💡 Code Analysis Proof:

Based on RedShell’s own backend code, referral bonuses are taken directly from the deposit of your downlines, NOT from actual crab sales.

This is a major pyramid scheme indicator.

To answer that, we need to understand real crab fattening in the Philippines.

| Season / Price Level | Buying Price (₱) | Selling Price (₱) | Profit (₱) | ROI (%) per Cycle |

|---|---|---|---|---|

| Normal – Low | 400 | 1,000 | 600 | 150% |

| Normal – High | 400 | 2,000 | 1,600 | 400% |

| Peak – Low | 400 | 2,300 | 1,900 | 475% |

| Peak – High | 400 | 2,400 | 2,000 | 500% |

These are the best possible selling prices under ideal conditions, but not consistent all year round due to market fluctuations, mortality, disease outbreaks, and seasonal demand — and this still does not include production costs or the initial investment required to build and operate a crab farm.

In real crab farming:

One of the biggest sustainability issues: RedShell has no cap on the number of investors.

Based on actual production capacity from a 1,000-box crab farm, here’s the maximum sustainable investors before payouts exceed actual farm profit:

With no investor cap, once the number of investors exceeds the farm’s real production capacity, the only way to pay old investors is from new investor deposits — the core mechanism of a Ponzi scheme.

In real-world crab farming, even in efficient large-scale operations, 42%–66% annual ROI is realistic — nowhere near these figures.

Crabs do not fatten in a single week — the minimum cycle is 15 days for males and 30 days for females.

If RedShell is paying weekly, it means investors are getting paid before any actual harvest happens.

Analysis of RedShell’s website code shows that referral payouts come from deposits made by new members, not from crab sales.

This is a hallmark of pyramid/Ponzi schemes.

No legitimate agribusiness can guarantee both your full capital and fixed profits.

Real crab farming faces mortality risk, disease outbreaks, typhoons, price crashes, and market delays.

In real crab farming:

A fixed return of 2%, 4%, 120%, or 1,000% ignores all these realities and is a clear sign it’s not tied to genuine farming operations.

If one investor puts in ₱100,000 and earns 4% weekly → that’s ₱4,000 in weekly payouts.

If there are 100 such investors → ₱400,000 in weekly payouts.

If the profit per kilo is ₱2,000, they would need to sell 200 kilos per week — that’s 10,400 kilos per year.

This would require a massive crab farm — which RedShell has not shown evidence of owning or operating.

If you’re thinking of investing in RedShell, think twice.

Real crab farming can be profitable, but not through guaranteed fixed weekly returns — and definitely not in a scheme that depends on new investor money to pay old ones.

💡 Recommendation: Avoid this investment. If you want to get into crab farming, do it directly and manage your own production, where you control the risks and rewards.

ADA or Apex Digital Academy is now everywhere on TikTok and Facebook.

It’s quite difficult to find information about this program because most of its details are hidden. You actually have to purchase their online course before you can fully understand what they’re really offering.

This lack of transparency raises questions, so in this review, I will share everything I found out about ADA, based on my own observations and experiences.

Based on videos circulating on TikTok and Facebook, Apex Digital Academy is an online training program that offers digital skills training and opportunities to earn through social media and affiliate marketing.

In short, it’s presented as an online course that will supposedly teach you “legit ways to earn money online.”

According to their official Facebook page, they position themselves as a “One Stop Online Business Solution.”

ADA has a two-tiered program:

Let’s start with the entry course first.

When you buy the entry-level course, you get four videos. But here’s the big question:

Do you actually learn something useful?

This video shows success stories of students who enrolled in the advanced course.

Examples: Some were allegedly interviewed by radio programs, and others claimed to have earned six figures after joining the advanced course.

Observation:

For me, this video doesn’t really teach practical skills you can use right away. It felt more like hype-building for the next videos and the advanced program.

This video talks about struggles like:

Observation:

It’s ironic because the video also mentions “Investing in the Wrong Business or Scam Schemes” and asks “Have you been a victim of networking?” – yet ADA’s advanced course is actually tied to a networking-style affiliate system (more on that later).

This video introduces:

Observation:

This was very basic. You can find the same information for free on YouTube. In fact, many YouTubers teach these topics in detail and for free.

For the ₱990 you spend on ADA’s entry course, you could enroll in a more structured, advanced, and clearer course on platforms like Udemy – often for the same price or cheaper.

This video focuses on:

Observation:

This part was a bit contradictory. In Video 3, they introduced those business models. But in Video 4, they dismiss them as inferior and say ADA is the better option.

It would have been clearer if they had just presented ADA directly instead of spending time introducing other models only to discredit them later.

For me, the real purpose of the four videos is to upsell the advanced course.

You pay ₱990 not to learn real skills but to be funneled into their sales process.

This is what I would describe as a “bait-and-switch” pattern (my opinion based on what I saw):

Other red flags in the entry course:

If you decide to upgrade, you’ll get access to the Advanced Mastery Program, which includes:

Price:

Once you join the Advanced Mastery Program, your affiliate dashboard, e-wallet, and “income protection” features are tied to Ascendra International, which is in partnership with ADA.

This partnership was confirmed in a post dated July 1.

While ADA advertises itself as a digital skills training program, in the end, it heavily relies on a recruitment system connected to a networking-style structure to generate income.

Here are the major red flags I observed:

Based on my experience, I do not recommend APEX Digital Academy.

It is a high-risk program with questionable marketing practices, and the training value is not proportionate to the cost.

There are many other online courses available (like Udemy or Skillshare) that are:

Avoid ADA if you are not fully aware of the risk and if you’re not prepared to spend a large amount just to get started.

Look for a program that is:

What do you think after reading this review?

Comment your thoughts below. Your feedback can help others decide whether or not to join ADA.

APEX Digital Academy is not recommended.

It may seem promising on the surface, but the structure is highly focused on upsells and recruitment rather than real skills training.

If your goal is to genuinely build your skills in freelancing, affiliate marketing, or digital business, you’re better off investing in programs that are affordable, transparent, and skills-based.A?

Do you see it as a legitimate program or a high-risk funnel? Share your thoughts in the comments – your insights can help others decide.